Articles & Questions

Every week I publish a fun new article on a money topic I think you’ll find interesting. I also answer a handful of reader questions. Subscribers to my newsletter get to see everything first — but you can browse some of my past articles & questions on this page.

My Best Articles

Not sure where to start? Below I’ve handpicked a few of my favourites. And if you like what you see, don’t forget to subscribe to my free newsletter to get new issues before anyone else!

Search Articles

Our Tenant Burnt Our House Down

Hi Scott, Our tenant burnt our investment property down (has been charged with arson). The property has landlord insurance for $500,000.

Hi Scott,

Our tenant burnt our investment property down (has been charged with arson). The property has landlord insurance for $500,000. The insurance company has offered us $309,000, or to rebuild it themselves. They’re also being a bit suss on paying us for lost rental income. Our mortgage is around $380,000, but the block will also need to be cleared. Is there any way we can get the $500,000 we are owed, or close to it?

Tammy

Hi Tammy,

You may be insured for $500,000, but the fine print in your policy may say that all the insurer is required to do is reinstate you to the same condition you were in before the fire. And if they can get away with paying out $309,000 instead of $500,000, that’s what they’ll do. You’ll need to read your policy carefully to see what it says.

Remember though your policy was written by the insurance company lawyers, with the aim of giving them maximum wriggle room. That doesn’t mean you shouldn’t challenge them -- especially on the loss of rental income. You have nothing to lose, and everything to gain.Let your insurer know that if don’t get a satisfactory outcome, you’ll register your complaint with the Financial Ombudsman Service (1800 367 287). After that your insurer has 45 days to resolve your complaint.

Scott

Helping Out My Mum

Scott, At the age of just 30, I am VERY aware of the importance of super. Here’s why.

Scott,

At the age of just 30, I am VERY aware of the importance of super. Here’s why. My mum is two years off the pension and has $8,000 in super. Yep, not a typo. I am going to ‘gift’ her $200,000 or so from the sale of my house (I have another, so will not be homeless), and she will be able to buy a house on which she will owe nothing. I have two questions for you. How might this ‘gift’ affect us? And how can Mum, who works full time earning $40,000 a year, maximise her super in the two years of work she has left?

Tracy

Hi Tracy

I hope my daughter looks after me as well as you do for your mum!

First up, let’s look at what you’re trying to achieve: you want to put a stable roof over your mum’s head so she has a sense of security and doesn’t have to worry about moving.

If I were in your shoes, I wouldn’t just give her the cash.

Instead, I’d consider buying an investment property in your name and renting it out to her.

There are three advantages to this:

First, when she goes on the age pension she’ll get rent assistance ‒ the maximum payment is $134.80 per fortnight.

Second, as long as it’s an arms-length transaction, you’ll be able to claim the interest and related expenses of the property against your tax, like any other investor can.

Third, it makes things a lot simpler. You should have a written tenancy agreement that sets out who pays for what, and what upkeep she’s expected to do, just like you would for any other tenant. That’s not only going to help you prove this is an arm’s-length transaction, but also manage everyone’s expectations. Also, in the event of her passing, the property is yours and is separate to her estate.

Now, as far as how your mum should manage her money over the next few years before she retires, here’s what I’d suggest if it was my mum:

When she retires she’s going to live on $23,597 per annum (the maximum pension for a single person, not including rent assistance and the health care card, worth at least $1,500 a year).

I’d encourage her to be a ‘practice pensioner’ – by living off that figure now and saving the rest of her wage.

Her aim should be twofold:

First, to have a goal of at least $100,000 in super when she finishes full-time work in five years (not two!).

Second, to never retire … keep working part time at least a day or so a week, and supplement her pension by up to an additional $6,500 a year (which, thanks to the Budget, will increase to $7,800 on 1 July 2019).

The upshot is that you’ll have an investment property with a great tenant. Your mum will have the security of a home, plus $100,000 in super to draw on, and she’ll be earning more in retirement (after tax) than she is right now!

Of course, you should run this past your accountant and financial advisor, but that’s how I’d do it.

Scott

Robbed with a Pen

Dear Barefoot, Five years ago we were advised to start up an SMSF and buy a property within it. We bought a unit for $400,000, for which we had to borrow $275,000.

Dear Barefoot,

Five years ago we were advised to start up an SMSF and buy a property within it. We bought a unit for $400,000, for which we had to borrow $275,000. Since then the value of the unit has dropped by more than 30 per cent ‒ it is now valued at $260,000! Our monthly super contributions are sucked into the property as the monthly rent does not cover the mortgage and expenses. Should we continue as we are and hope the property value increases over the next few years, or sell and start rebuilding our superannuation from scratch?

Dave

Hi Dave,

You got robbed with a pen, you poor bastard.

If someone walked into your home and stole $40,000 off your kitchen table, they’d be locked up for larceny.

Yet most of the spivs that market these SMSF schemes trouser up to $40,000 in commissions.

They know the apartments they’re flogging are horribly overpriced, and that they’ll eventually blow up their client (which is why they often advise their clients to “never, ever, sell” ‒ because if you never, ever, sell, you’ll hopefully never, ever work out you’ve been ripped off).

But these guys don’t go to jail, they go to Italy ‒ first class.Research firm Rainmaker says the true cost of fraud over the last decade from SMSFs is a staggering $103 billion, once you include the loss of investment returns from no longer having the money to invest.And that’s precisely where you are right now.

Your new super contributions are being eaten up by a loss-making property that you hope will come good. But hope isn’t a strategy, Dave. Besides, in all the years I’ve been doing this, I’ve never seen time turn a bad property into a good one.

So let’s deal with the facts: you were flogged an overpriced property that was never worth the $400,000 you paid.

If I were in your shoes, I’d sell the property, and begin again ‒ this time in an ultra-low-cost industry super fund.

The clock is ticking, Dave. It’s time for action.

Scott

Too Good to Be True?

Dear Scott, A friend has signed up with an investment company where they have set up a self-managed super fund (SMSF). This group uses this money to buy him investment properties, which they buy and then run.

Dear Scott,

A friend has signed up with an investment company where they have set up a self-managed super fund (SMSF). This group uses this money to buy him investment properties, which they buy and then run. It has not cost him a cent other than his super. He thinks this is a great retirement plan. We are middle aged and trying to get ahead for retirement. We have a big house (in a ‘povvo postcode’), a blended family of five kids, and a huge mortgage ‒ and we feel trapped! Is my friend’s experience too good to be true? Help!

Alison

Hi Alison,

Well this sounds like a thoroughly bad idea.

He claims “it has not cost a cent other than super”.

Well, unless his super consists of cans of Pal Meaty Bites, I’d suggest it is in fact a nest egg that he needs to grow to a sufficient level by the time he retires ... so he doesn’t end up eating dog food in his golden years. And if he’s investing in a scheme like this, it’s highly likely he’ll end up eating home-brand dog food (the stuff even my sheepdog rejects because it gives her gas).

Okay, enough of the dog jokes.

Alison, I want you to call your friend and invite him over.

Boil the kettle, pour yourselves a cuppa and, together, read the next question.

Scott

Million Dollar Payday

Dear Scott, I am 24 years old and I earn $40,000 a year working part time. Today I received a lump sum of $1,000,000 (after costs) due to being run over by a car seven years ago.

Dear Scott,

I am 24 years old and I earn $40,000 a year working part time. Today I received a lump sum of $1,000,000 (after costs) due to being run over by a car seven years ago. I need to pay around $5,000 a year in ongoing medical costs. How should I invest this money, and is it worth setting up a trust and a ‘bucket company’ that reinvests in itself?

Max

Hi Max,

First up, you won’t have to pay tax on the payout itself, but you will pay tax on any investment earnings you earn on it. Now, would I invest the money in a trust and then distribute the investment income to a company?

Possibly. The trust will give you asset protection benefits, and the company acts as a ‘bucket’ to theoretically cap your tax rate at the company tax rate of 30 per cent. But know this: it’ll also gobble up a few thousand dollars a year in fees to your accountant.

However, let’s not put the cart before the horse.I

f I were in your shoes, I’d keep it simple:

I’d buy a nice little unit for cash (say $500,000).I’d put $15,000 into Mojo (high-interest online saver account).

I’d put $25,000 into term deposits with different maturities to cover any medical costs within the next five years.

I’d also kick $25,000 into your super.

Then I’d invest the rest ($435,000 or thereabouts) into good-quality Aussie shares (either via a trust, or in your own name), tick the ‘Dividend Reinvestment Plan’ option (so your dividend earnings are automatically reinvested rather into more shares), and let your money compound.

Scott

Should I Sell My Investment Property?

Scott, I’m torn! Back in 2008 I bought my first home for $126,000.

Scott, I’m torn!

Back in 2008 I bought my first home for $126,000. I have paid it off since then and started renting it out in 2012, when I moved into my husband’s home. My rental property is now worth about $150,000 and, to be honest, I do not think it is ever going to rise much in value. The only upsides are that it is relatively easy to find tenants for it ($220 per week) and I make about $5,000 a year from it. I am considering selling and using the proceeds to invest in shares, and to renovate our home. Or should I just keep it? It would be nice to rent it to a single mum with four kids!

Ally

Hi Ally,

What an awesome achievement!

In years to come, how powerful would it be to show your kids -- especially your daughters -- the home that Mum saved up and bought on her own, before she met Dad? Who cares if it’s a poky little joint? Stories are powerful, especially for kids.

Having said that, if you’re not emotionally invested in the property, I’d probably sell it, cop the tax, and move on.

What tax?

Well, it’s likely you’ll be up for capital gains tax (CGT), though you’ll only pay it on any gain you’ve made since 2012 (when you moved into your current home). Better yet, that capital gain will be further discounted by 50 per cent as you’ve held the property for over 12 months.

So why sell?

Well, you’re already questioning the likelihood of future capital gains, and you wouldn’t hold on to it just for the 3.3 per cent rental yield ($5,000 a year). Besides, let’s face it, being a landlord can be a triple pain in the rump -- hello renters, repairs, and real estate agents.

If I were in your shoes, I’d sell the place, make a tax-deductible donation to a woman’s shelter in your area, spend as little as I could on renos on your current home, and put the bulk of it into super.

Scott

Burning Through the Bucks, Baby

Dear Barefoot, I am 35 and engaged to the most generous guy, who I love. But we have spent $31,000 in two months!

Dear Barefoot,

I am 35 and engaged to the most generous guy, who I love. But we have spent $31,000 in two months! We earn $330,000 p.a. combined and have equity of $850,000 in our two properties, which we will sell next year so we can get a nice home with a small mortgage. Recently I did an audit and found we had spent $31,000 on … nothing! Meals out, weekends away, events at home, clothes, bond, removalists, some double rent for a period. I want to be debt-free in five years. Kick us up the pants!

Amanda

Hi Amanda,

Honestly, on your income you probably don’t need a kick up the pants -- you’re going to be fine ...… so long as you continue earning $330,000 a year. But if the money dries up, things can go into reverse pretty quickly.

It’s a three-step trap that I’ve seen plenty of high-income earners -- doctors, lawyers, footballers -- fall into:

First, buy expensive toys (boats, cars, and cash-draining McMansions).

Second, spend like a Kardashian -- and only invest in money-losing ventures that ‘lower my tax!’.

Third, get hit with one of the big D’s: divorce, disease, disability … or a downturn where you lose your income.

It’s more common than you’d think: recent research from Digital Finance Analytics (DFA) found that 30,000 households living in wealthy suburbs like Sydney’s Vaucluse (median price $4.5 million) and Melbourne’s Brighton (median price $2.6 million) are at risk of defaulting on their debts.

Truth is, wealth isn’t what you earn, it’s what you save.You want to impress me?

Don’t humblebrag about the $31,000 you’ve peed into your Prada handbag over the past couple of months.

As financial philosopher Shania Twain says, “That don’t impress me much”.

Instead, buy a house you can afford, pay it off, then show me your plan for how you will eventually replace some of your income through passive income, i.e. your investments.

Thank-you for reading.

Scott

Centrelink Property Mogul

Hi Scott, I’m a 41-year-old single mum stuck on Centrelink benefits. I cannot work for health reasons, but I love (and have always loved) houses!

Hi Scott,

I’m a 41-year-old single mum stuck on Centrelink benefits. I cannot work for health reasons, but I love (and have always loved) houses! I am cashflow poor but have a good amount of equity in my home and want to work towards having two or three properties to support myself and provide for my future. I have found a few cheap, positively geared properties I could buy with the equity, but once their value reaches $250,000 my benefits would be cut. Any advice on how to get out of this cycle?

Natalie

Hi Natalie,

I love that you want to get off the welfare cycle … but you’ll be replacing it with a debt cycle.

Now, even though you have equity in your home, and you’re planning on buying cash flow-positive investments, the banks are bound by responsible lending laws to take your income into account.

And if you’re on Centrelink, you don’t have enough income.

My view?

If you’re smart enough to hunt down positively geared investments, then you should be able to turn your talents to doing paid work in some capacity. And working is the only surefire way to escape the welfare cycle. You’ve got this!

Scott

Where to Invest $5 million?

Scott, My wife and family are in a very fortunate position after selling our business in February this year. We have no debt, own our house valued at $5,000,000, own a beach house valued at $1,700,000, super $1,700,000, and approximately $5,000,000 in cash.

Scott,

My wife and family are in a very fortunate position after selling our business in February this year. We have no debt, own our house valued at $5,000,000, own a beach house valued at $1,700,000, super $1,700,000, and approximately $5,000,000 in cash. We have sourced some advice on how to invest the $5,000,000 to provide an income stream of hopefully around 5 to 6 per cent per annum (they have suggested buying a commercial property and some investment properties). We now have financial advisors all over us like wet dogs. What would you do?

Gary and Helen

Hi Guys,

Congratulations on your success!

To get rich you will have concentrated your risk, and focussed all your effort into one business. However to stay rich you need to do the exact opposite: spread your money across a large number of investments, and take very few risks.

Therefore I’d run away from all the wet shaggy dogs that are trying to gnaw on your juicy assets. They have dollar signs in their eyes. Also, stay away from anyone who is recommending you invest directly in commercial or residential property. Reason being, it’s simply not diversified enough, and if you lose a tenant, you lose your yield!

Look, you’ve earned the right not to have to worry about your money. So if I were you, I’d keep a hefty amount of in cash (for opportunities, and because a $5 million home sounds kind of expensive to maintain!), and invest the rest in a broad mix of shares (local and overseas), via ultra-low cost index funds. The income you generate from dividends should be enough for you to live off without having to draw down on your capital.

Finally, you say that you’ve got got $1.7 million in superannuation, however, the cap is actually $1.6 million per person, so you may have the ability to contribute more. If you can, you should.

Scott

The Chicago Bull

Hi Scott,I have a terrible credit rating. I'm 45 and only have a couple of thousand dollars in savings, and $6k in super.

Hi Scott,

I have a terrible credit rating. I'm 45 and only have a couple of thousand dollars in savings, and $6k in super. I also have have $15k in credit card debt. I earn $800 a week. My question is, when is the right time to enter the housing market?

Chris

Chris,

You’re like a middle-aged tubby little fella limbering up to have a crack at the NBA! Dude, you’ve got no savings, fifteen grand in plastic, and you’re earning below the average wage. Right now you’ve got as much chance of buying a house than being drafted to the Chicago Bulls. So let’s keep it real. You first need to increase your income, then knock out your debts, build up your savings, and only then will you be ready to shoot for the stars.

Scott

Paid Off the House … What Next?

Hi Scott, My partner and I both turn 32 this year, and by January 2018 we will have our home paid off in full, all on a combined $150,000 a year. We are already thinking ‘what next?

Hi Scott,

My partner and I both turn 32 this year, and by January 2018 we will have our home paid off in full, all on a combined $150,000 a year. We are already thinking ‘what next?’ and would appreciate your advice. We think we will both put an extra 10 per cent of our wages into super, build up our Mojo, and save for an overseas trip. We are also considering buying an investment property or getting into the share market. And one more thing: we intend to start a family in the next year or two. Where is the best place to put our money?

Ella

Hi Ella,

O.M.G.

You paid off your home in your early 30s?

If you were standing in front of me, I’d give you both a big bear hug. Better yet, let your family and friends give you one -- plan one hell of a par-tay for January 2018! Seriously, paying off your home is one of life’s great achievements. Celebrate it.

(For anyone keeping score at home, you’ll notice that Ella gave the month she would be debt free. She’s focused on her numbers. This didn’t happen by accident.)

Okay, so what should you do now?

Well, first, avoid the Instagram-envy of thinking you have to trade up to a more expensive home. The ultimate status symbol isn’t a flashy home or car -- it’s having the freedom to travel and spend quality time with your kids (when you have them!).

Being debt-free at such a young age, you can’t help but become incredibly wealthy. I’d suggest you go through the Barefoot Steps: boost your pre-tax super contributions, and build up your Mojo to cover three months of expenses (which will be much less without a mortgage). Then, I’d look at setting up a family trust and investing in low-cost share funds (consider buying an investment property when the market crashes). If you’re able to invest just $30,000 a year, you’ll be looking at a nest-egg worth over $5 million by the time you retire.

Scott

If you want to buy a cheap inner city apartment … read this

Tick. Tick.

Tick. Tick. Tick.

That’s the sound of the inner-city apartment market.

There are 15,000 brand-spanking-new apartments due to settle before 30 June this year.

Many of these apartments won’t settle … because the buyers can’t come up with the balance of their money, after paying a deposit.

A couple of years ago I wrote a click-baity story:

“2018: The Year First Home Buyers Get Their Revenge!” (Not bad eh?)

I was writing about the opportunity for first homebuyers to buy a brand new inner-city apartment — at fire sale prices. Much, much cheaper than they were selling for at the time.

Here’s what I wrote: “In three years’ time there will be an oversupply of inner-city apartments in many parts across the country. It’s actually not hard to forecast today, because we can see what’s coming down the property pipeline in a few years’ time: apartment towers take years of planning and regulations to get approved. When the market is hot, like it is now, lots of developments spring up to feed the demand … but there’s a lag.”

Basically, I argued that too many investors had put down too little a deposit, and when payment was due they’d struggle to come up with the dough — causing them to either default with the developer, or sell at a massive loss.

Today I want to revisit that topic, to see how we’re faring.

Blood in the Streets

The housing boom has been fuelled by property investors, and in inner-city apartment markets it’s been driven by Chinese investors buying up big.

So this week I caught up with Li Ming, a co-director of Aussiehome, who specialises in selling Aussie property to Chinese investors.

Ming: “The Melbourne off-the-plan apartment market is the worst I have seen in the last 10 years.”

Barefoot: “How long have you been in the market?”

Ming: “5 years.”

Ming believes that around 80% of Chinese buyers won’t be able to settle on their Australian apartments.

So what’s happening?

Well, Chinese investors are caught in a ‘pincer grip’.

Here’s a real-life example of one of Ming’s clients:

Three years ago his client bought a yet-to-be-built, off-the-plan, two-bedroom apartment in Melbourne’s Southbank for $750,000.

They put down a $75,000 deposit (10%) and planned to organise a loan for $675,000 (90 per cent) in three years’ time when the apartment was built.

Now, at the time his client was flipping through the glossy apartment brochure Melbourne prices had soared 35% in the three years prior … so there was a chance the investor could turn around and sell the apartment for more than $1 million by the time the apartment finished.

Yeah, Nah.

Let’s get back to the present day.

The Pincer Property Grip

Because of the oversupply of inner-city apartments, the Aussie banks are now being cautious about how much they’ll lend (and they’re also charging investors a higher interest rate for their loans). They told Ming’s client they wouldn’t stump up 90% of the purchase price — only 80%.

Remember, Ming’s client was still contractually bound to pay $750,000 to the developer.

Bottom line: he was $75,000 out of pocket.

So where does he find the extra money?

Well, that’s the second part of the pincer grip: the Chinese Government.

For the past year, the Chinese Government has been clamping down on investors taking money out of this communist country. Investors used to be able to take out $US50,000 per person per year … yet now many state-owned banks are lowering the amount, or outright blocking the money going overseas.

“So what did your clients do?” I asked Ming.

“They had no choice. They walked away … and lost their $75,000 deposit.”

Ming told me he has other clients who flat-out couldn’t get finance from the banks.

“They managed to negotiate to flip their apartment for a 7% loss … but even that is getting harder to do. Everyone is getting desperate”, he said.

60 Minutes Says …

Australia’s ‘flagship’ current affairs program, 60 Minutes, did a story last week on housing affordability. They interviewed two of our biggest inner-city apartment developers about the issue.

However they didn’t press them on the fate of Chinese investors. They didn’t ask what effect the banks repeatedly jacking up interest rates on investors was having on demand. And they certainly didn’t ask why the Reserve Bank has openly stated this week that it’s worried about the inner-city apartment market … along with flat-as-a-pancake wages growth, heavily indebted households, and sluggish growth.

Instead, they simply walked around in hard hats, grinned, and pointed at skyscrapers. And, in turn, the two rich white dudes gave two bits of incredibly condescending advice to young first homebuyers:

“Suck it up” and …

“Let us build more apartments.”

Seriously, that’s what they said.

Angry Millennials took to Twitter to vent their frustration about being labelled unrealistic, coffee-swilling, avocado-eaters.

My advice?

Don’t get angry … get even. Falling prices are coming, and right on cue.

Tread Your Own Path!

A Brick to the Head

Hi Barefoot, I have been thinking about what I could do to have my deposit savings keep pace over the next couple of years before I buy my place. One idea I have is to invest my deposit savings into BrickX, which allows you to buy a share in an investment property.

Hi Barefoot,

I have been thinking about what I could do to have my deposit savings keep pace over the next couple of years before I buy my place. One idea I have is to invest my deposit savings into BrickX, which allows you to buy a share in an investment property. I see it as a hedge against rising property prices. What do you think?

James

Hi James,

I wouldn’t do it, even though it is a hedge (less their fees, and less any potential capital gains tax).

Reason being, I don’t advise people to buy an investment property before they purchase their principal place of residence, because in all the years I've been doing this I’ve never seen it work out. (And with a BrickX property, you don’t have the option of eventually living in it.)

ScoMo’s new ‘First Home Super Saver Scheme’ is admittedly a bit of a fizzer (maybe that’s why it’s got the acronym FHSSS)?

But it’s exactly where you should be saving for the last few years of your deposit. That’s because a couple earning $65,000 each will save an additional $12,000 by using the scheme -- guaranteed. And for the average Aussie trying to buy a home in one of the most overvalued patches on earth, every cent counts.

Scott

Aggressive Wealth-Builders Go for Broke

Dear Barefoot, My husband and I are in our early 30s and we earn $175,000 combined. We are aggressive wealth-builders.

Dear Barefoot,

My husband and I are in our early 30s and we earn $175,000 combined. We are aggressive wealth-builders. However, one of our investment properties is in negative equity by $75,000 (we had a loan to value ratio of 97 per cent). We have no way of refinancing or selling as we cannot cover the shortfall currently. We have three other investment properties (one that we will move into in five years) and thought to sell them to cover the shortfall. However, we have just had independent valuations done and this would only cover $20,000 -- a huge mess! Do we direct our ‘fire extinguisher’ money to this and pay it down to where we can sell it? I say yes, partner says no. HELP!

Stacey

Hi Stacey,

Aggressive is one word for your situation. Borrowing 97 per cent of the value of the property doesn’t leave you with any wriggle room (negative equity simply means you owe more on your mortgage than the house is worth, in your case to the tune of $75,000).

I understand the concept of aggressively using the equity to ‘leapfrog’ and buy more investment properties. There are entire books devoted to the strategy, and they all end with the landlord becoming filthy rich. In the book, that is.

The ‘only’ thing you need to watch out for is going broke in the process! To avoid that, you need a buffer.

So let’s talk about your buffer. You need to make sure that you have enough money to cover the impact of higher interest rates, prolonged vacancies, and maintenance costs. That’s just for the investments. You also need Mojo (and income protection) in case one of you can’t work.

Either way, I’d be aggressively saving -- and then potentially looking at unwinding the strategy.

Scott

Divine Intervention

Scott, Could this be divine intervention? I have just read your recent article in which you saved a single mum from a property ‘guru’.

Scott,

Could this be divine intervention? I have just read your recent article in which you saved a single mum from a property ‘guru’. It hit home for me because my husband and I are considering signing up for one of these programs -- a ‘step-by-step guide’ to investing in commercial property. It is not the $17,000 your article mentioned, but it is still $3,000 that we do not have and which we are considering paying for on our credit card.

My husband is excited and wants to go ahead, but I am sceptical. We follow your blogs, have read your book, and religiously read your articles in the paper. In the past you have advised that commercial property is a good investment, though you were referring to shares in commercial companies. We know a little about investing in property (having bought a property through our SMSF which seems to be going well), but we are scared to take the plunge. What would be your advice?

Natalie

Hi Natalie,

Tell your husband to pull his head in. You should both have an equal vote on where you spend your money. You’ve voted ‘no’ for what I think are intelligent reasons -- the biggest of which is that you don’t actually have the money to buy the course. Anyone who buys a $3,000 course on credit card should not be investing in commercial property!

Scott

When will the housing market crash?

Donald Trump reminds me of the bullies who teased me at school. Anyone who stands up to him gets a put-down: ‘Crooked Hillary’, ‘Little Marco’, ‘Low Energy Ted’.

Donald Trump reminds me of the bullies who teased me at school.

Anyone who stands up to him gets a put-down: ‘Crooked Hillary’, ‘Little Marco’, ‘Low Energy Ted’. His aim is to get everyone laughing at them, just like in a classroom.

And like all bullies, he only wins by getting you to doubt yourself -- rather than getting you to believe in him.

And that’s because it’s hard to believe in Trump.

He’s a liar. He cheated on his wife(s). Heck, he even wrote a book with the ‘Rich Dad, Poor Dad’ guy (Robert Kiyosaki) entitled Why We Want You to Be Rich -- ironic, given the authors have notched up five corporate bankruptcies between them.

And yet, in this week’s presidential debate, the ‘Big D’ actually said something intelligent:

“We’re in a bubble right now, and the only thing that looks good is the stock market. But if you raise interest rates even a little bit, that’s going to come crashing down. We are in a big, fat, ugly bubble. And we better be awfully careful.”

Okay, so only a shrink can fully explain why Trump feels the need to label everything ‘big, fat, and ugly’ ... yet he’s right on one thing: we are in uncharted financial territory.

Right now, global interest rates are the lowest they’ve been in recorded history. In fact, in many countries interest rates are negative. Since the dawn of civilisation savers have earned interest, borrowers have paid it. That’s now been flipped.

Park the fancy economic talk and think about how ultra-low interest rates are affecting you:

Interest rates are the main reason your house value has increased so much. People aren’t earning more -- they’re just borrowing more. That’s how Australia wound up with some of the highest levels of household debt (compared to income) in the Western world.

And ultra-low interest rates are forcing retirees out of (safer) fixed interest and cash accounts, which pay two parts of bugger all, into the (riskier) stock market to earn dividends.

When interest rates go up, as they surely will, the bubble will burst -- and house prices will come down.

Here’s you: ‘Dude! When will that happen?’

Here’s me: ‘I have absolutely no idea, and neither does anyone else. Not even the comb-over king.’

Here’s you: ‘So what should I do in the meantime?’

Here’s me: ‘Read on.’

When Will the Housing Market Crash?

I’ve been the Barefoot Investor for 15 years. And for all that time I’ve been warning about our unsustainable debt levels. However, in that time I also bought my family home.

At the time I bought, I was convinced the market was overvalued. But I was sick of renting, and I fell in love. And history had taught me that prices can remain overvalued for many, many years.

Besides, no one can predict the future. As the excellent book Future Babble, by Daniel Gardner, proved, the more famous the forecaster, the more likely they’ll be as accurate as a dart-throwing monkey.

The truth is that there are no answers.

That’s why I saved up a 20 per cent deposit, and factored in a repayment interest rate of 10 per cent. And then I set about working my arse off to get the banker off my back, once and for all.

And lo and behold, over the years, interest rates halved, and the joint doubled in price.

Things could just have easily have gone the other way, of course. After all, I don’t have control over house prices. Or the direction of interest rates. And that’s why I didn’t bet on any of this happening.

I just bet on myself.

When Will the Share Market Crash?

Back in January, things looked grim.Wall Street had the worst start to the year on record.

The esteemed Royal Bank of Scotland’s dedicated analysts ... cracked.They told their clients to prepare for a “cataclysmic year”.

It made global headlines, and freaked everyone out with their bone-chilling recommendation:“Sell everything”.

Hold your haggis!

Truth is, scary headlines are good business, especially when they coincide with a market going down (remember that old adage, ‘if it bleeds it leads’). And besides, in an era of 24-7 tweets, and Brad and Angelina, no one ever has time to go back and check what they said.

So let’s do that.The Royal Bank of Scotland predicted that markets could drop by a fifth, and that oil could drop to $16 a barrel.

How’s that call looking today?

Well, oil is up 40 per cent, emerging markets are up 29 per cent, the US S&P 500 is up 14 per cent, US high-yield bonds are up 13 per cent, and even the ASX 200 is up 10 per cent.

Look, I’m not talking a potshot at a bloke in a kilt.

All I’m saying is that you could be right about a crash in the market, but wrong about the timing. And the upshot is you could be left blowing your bagpipes while the market doubles or triples.

So what can you do?

Well, when all else fails, use common sense.

I’ve long advised people heading to retirement to go from having three months of living expenses to having three to five years of living expenses by the time they retire. That gives you time to ride out the inevitable downturns. The rest of your money should be invested in good-quality shares that will keep your nest egg growing faster than inflation.

Finally, recognise when you’re getting played. One of the oldest tricks in the book is to prey on people’s fears. It gets people to do irrational things -- like voting for a big, fat, ugly orangutan.

Tread Your Own Path!

The Forty Thousand Dollar Phone Call

“NOW it’s mortgage brokers facing digital disruption in the third wave of property finance.” I read that headline earlier this week in much the same way that my three-year-old reads his bedtime stories.

“NOW it’s mortgage brokers facing digital disruption in the third wave of property finance.”

I read that headline earlier this week in much the same way that my three-year-old reads his bedtime stories.

By guessing.

“Mortgage brokers facing digital disruption” … hmmm, OK, so maybe it’s like Uber for home loans?

“The third wave of property finance” … OK, nope. I have absolutely no freaking idea what that means.

But it’s my job to understand, so I kept reading.

Turns out the article was about a new mortgage broking app called Uno, which allows the public to broker their own deals.

It’s the creation of a clever bloke named Vincent Turner, who, some years ago, actually developed the software that 90 per cent of Australia’s banks and brokers use.

Interesting.

Now he’s turning the tables on the industry by “providing home loan customers with the same screens that are used by mortgage brokers”.

“We are establishing the third major wave in the property finance industry: consumer-brokered home loans.”

Ahh, so that’s where the third wave analogy comes from.

“At Uno, we don’t like to think of ourselves as a mortgage broker. We don’t have a sales commission structure.”

Very interesting.

After all, the $1.3 trillion home loan market does need a bloody good shake-up.

About half of all home loans are set up through mortgage brokers.

The banks pay them a collective $2 billion a year in upfront commissions, as well as ongoing kickbacks for the life of the loan (which is why some brokers sign you up to a three-year fixed loan — it also fixes in their commissions).

The government is worried that conflicted commissions result in bad advice.

After all, under the commission structure, the more you borrow the more they make.

So I called Vince at Uno, to talk about the “third wave mortgage revolution”.

He had his pitch face on: “Look at any other vertical: real estate, jobs, cars … there’s been a disruptive, revolutionary platform that consumers embraced.

“ That hasn’t happened with mortgage brokers. The home loan market is ripe for disruption … and we intend to own that category.

“Once consumers understand that they’re getting a better outcome, you don’t need to advertise. People just flock to it.”

Flocking hell.

It all sounded very “fintech” to me. Very “our office has a ping pong table and the blokes who work here have beards and wear long pants without socks”.

When it comes to finance, you need to bypass the buzzwords and follow the money.

Barefoot: “So, what happens to all the kickbacks the banks pay you for lining up loans, cobber?”

Vince: “All the money goes back into the platform … to enhance the user experience.”

Barefoot: “What does that even mean? Oh! You’re trousering the commission’s, right?”

Vince: “Well, yes.”

Barefoot: “Dude, you’re about as revolutionary to the mortgage market as the Kia Rio is to the luxury car market.”

And there you have it. Strip away the fancy technology and it’s the same old flog.

Yes, I’m grumpy. And, no, my advice doesn’t change.

If you’re getting a new loan, you should look at the smaller, online lenders like UBank, which for years has consistently offered one of the cheapest no-frills loans for people buying with a 20 per cent deposit (and that should be everyone, in my opinion). They don’t pay commissions because they’ve got Aldi-like pricing, 3.74 per cent at the moment.

There are other lenders, that occasionally offer sweet rates to win new business.

If you want to go with one of them, you should go through a cashback broker, who will rebate the trailing commission they receive (but keep the upfront).

Do this over the life of your home loan and it can save you upwards of $40,000.

Here’s the thing: on a $500,000 loan, the banks pay brokers $3500 upfront and around $1500 a year to get your business. And that’s your leverage right there. That’s how much it costs the bank to replace you.

So, if you’re refinancing, the simplest thing you can do is to call your bank and put the hard word on them for a better deal. I’ve been saying this for years — and swear on my little fox terrier’s grave, it works.

Not a week goes by that someone, somewhere, doesn’t email, tweet or Facebook me telling me that they’ve rung their bank, bluffed that they’ve been offered a cheaper rate (usually quoting UBank’s rate) and saved themselves thousands.

Uno you should do it. Go on. And shoot me an email when you get a better deal.

Tread Your Own Path!

Reminder: I first wrote about this years ago and highlighted the low fees. Today there are better bank accounts on offer. How do I know? Because my readers constantly email me about them! So before you do anything, google the best accounts on offer now.

Australia's Youngest Property Owner

Picture this, it’s April 26. 3:30pm.

Picture this, it’s April 26. 3:30pm.

Malcolm Turnbull and Scott Morrison are deep in the ‘burbs.

The media pack is in tow, getting ready for a photo opportunity.

Today’s pitch? That negative gearing is the way everyday Aussies (voters) get rich -- and, unlike Labor, the Government won’t mess with it.

The Prime Minister peeks through the front door and surveys the battler family.

Turnbull: “He looks ethnic. She’s a blonde. They have a baby. All my ‘demos’ covered under one roof. Excellent.”

Sco-Mo: “Mal, before we go in … there’s just one thing … the apartment. It’s for the kid.”

Turnbull: “What?!”

Sco-Mo: “It’s negatively geared … for the one-year-old.”Turnbull: “Oh for christsakes. Who organised this sh…oot? It was one of Tony’s old staffers, surely?!

Sco-Mo: “It’s too late to back out now. The cameras are rolling. Just smile. It’ll be all over soon.”

A few awkward minutes later, and with the media money shot in the can, it was all over. Yet while there was a lot of fanfare, the only person who didn’t get their say was Australia’s youngest homeowner, baby Addison. So let’s fill her in with what’s going on.

A letter to Baby Addison

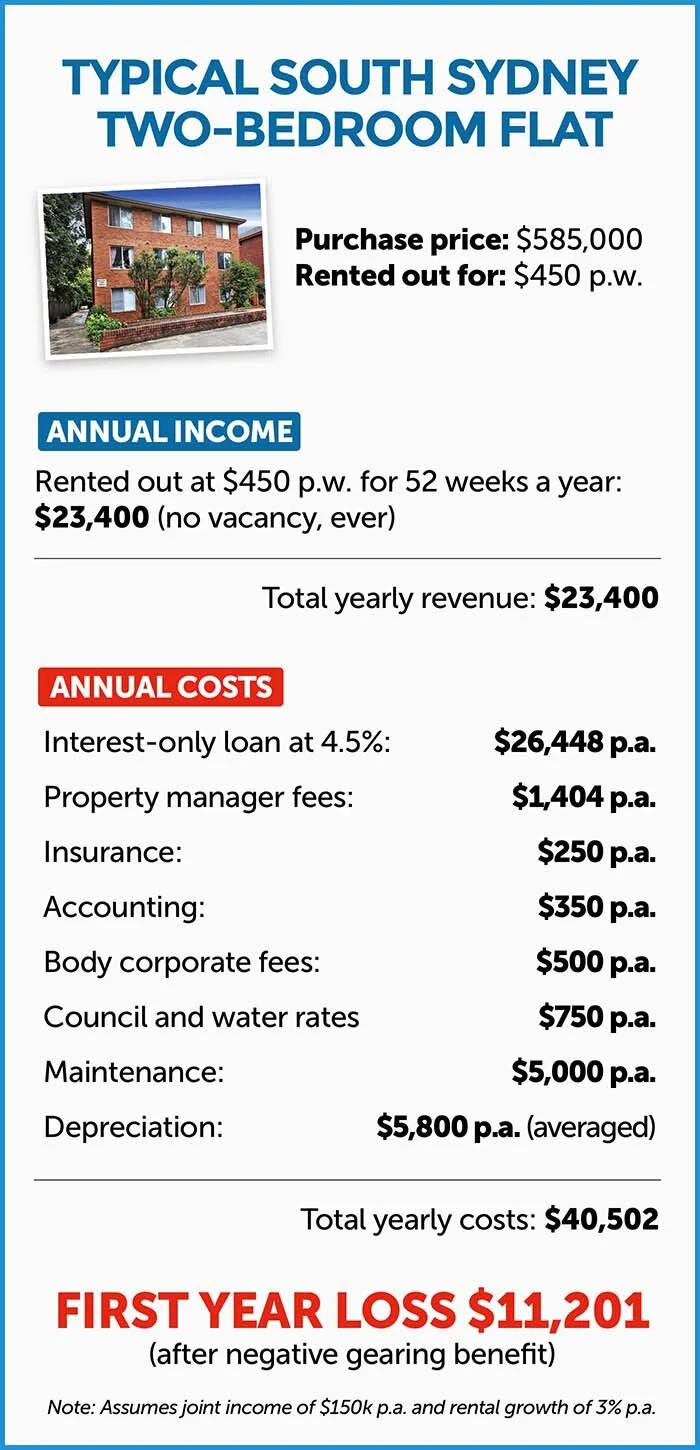

Dear Addison,

Your parents love you.When I was a one-year-old all I got was second-hand cigarette smoke, and a Melbourne Footy Club beanie. Your parents bought you a home!

Now, given you’re already crawling up the property ladder, it’s time we had a grownup chat about the true costs of being a property investor in 2016. See, despite interest rates being at all-time lows, your parents will actually lose money on your apartment every single year.

Let’s take a look at the numbers:

First, before your parents got the keys they had to shell out $22,144 in stamp duty, plus legals.

Then, even if we factor in healthy renting increases and an unlikely 100 per cent tenancy -- over the next 20 years they’ll lose $237,900 (see box).

Boo! Hiss!

Yet they’ll also get an annual negative gearing tax break, which will lessen their total after-tax losses to $155,800. Or, looked at another way, the hard-working nurse who delivered you (along with every other taxpayer) will chip in $82,100 over the next 20 years to help fund your loss-making investment.

So on very conservative figures, your parents will lose $178,944 over the next 20 years.

Now the majority of property investors today have absolutely no problem with that.But I do.I hate the idea of losing money every single year for 20 years -- even if I’m getting a tax break. Call me old-fashioned, but when I invest my hard earned money I expect my investments to put money in my pocket every single year.

And when I reinvest my returns each year, I’m getting something known as compound interest. Albert Einstein called it the eighth wonder of the world. That’s because, over time, you earn interest on your interest, and your returns snowball.

That’s the guaranteed way to get very, very rich.

But that’s not going to happen for you, unfortunately.

Your apartment won’t get the benefits of compound interest, because every last dollar of income (in the form of rent) that your parents receive, is completely gobbled up by your costs: to the bank, and to keeping the apartment. The only way your parents will make money is if the price of the apartment increases.

The Alternative: Create A Bond With Your Kid

But let’s be old-fashioned.

Instead of losing money each year, let’s save.

Now let’s run the numbers on investing the same amount that your parents will lose over the next 20 years in a low-cost, old-school investment bond, invested in an Aussie managed share fund.

For argument’s sake we’ll say your parents kick it off with $23,144 (what they paid in stamp duty and legal fees) plus what they lose (after tax) every year into the investment bond (which, as I’ve said, totals $155,800 after 20 years).

Assuming a conservative after-tax 6 per cent return, and annual investment fees of 0.78 percent, in 20 years your bond will be worth … $364,563.

A good deal for you, but an even better deal for your parents.

Here’s how I’d sell it to them, Addison.

“Mum and Dad, if you fund my future with savings, instead of debt, you’ll feel a lot less pressure. You won’t have to worry about losing your job, or not being able to fund the shortfall.”

(Which in the first year is approximately 10 per cent of your take-home pay.)

“You won’t have to worry about interest rates jacking up.”

(Let’s face it, interest rates won’t stay at a historical low for the next 20 years.)

“You won’t have to worry about your tenants breaking things, or leaving you in the lurch.”

(The figures we’ve used factor in a 100 percent tenancy over 20 years -- which won’t happen.)

“You won’t have to worry about greedy land tax grabs from the State Government.”

(They’ve got form here.)

“You won’t have to worry about changes to negative gearing.”

(Which, like changes to super, could change the game completely).

“You won’t have to worry about paying another round of stamp duty when you transfer the apartment to me in 20 years’ time.”

(Which will eat up another 4 per cent of your capital.)

“You won’t have to worry about paying capital gains tax at the end of it.”

(Investment bonds are totally free from capital gains tax free after 10 years.)

“So, Mum and Dad, for all these reasons I think you’ll agree it makes sense to save, rather than speculate. And besides, if you do, you won’t have set a precedent to buy my future brothers or sisters their own negatively geared apartment, which on these figures you won’t be able to afford … even with negative gearing!”

Tread Your Own Path!

Real Estate Mistakes: How to Turn $90,000 into $2.4 million

I’m writing this to you today from my study, which overlooks the rolling hills of my family farm. It’s really peaceful out here.

I’m writing this to you today from my study, which overlooks the rolling hills of my family farm. It’s really peaceful out here.

And, if you drive up to the top of those rolling hills, you can catch a glimpse of a smaller farm that’s just down the road, which was once marketed as Secret Valley.

“Set 45 minutes from the Melbourne CBD, the Secret Valley Estate is 258 acres of breathtaking, beautiful landscape and picturesque views of the Macedon Ranges.”

A few years ago, busloads of property investors would do field trips to Secret Valley.

They’d wander around the paddocks, sizing up what they were told was a canny investment.

The idea was simple: Secret Valley is on the edge of the Melbourne sprawl. Eventually it will be swallowed up by suburbia. And if you were smart enough to own an option on a few plots of land in the Secret Valley Estate, well, you could become very, very rich.

How rich?The marketing pitch that got the property investors on the bus was that if you invested $120,000 you could turn it into $1.2 million.

OK, so if you’ve been reading my column for a while, you won’t be surprised to hear that the investors in Secret Valley got roughly the same treatment that my ewes receive when I put a few daddy rams into the paddock.

A few years on, the only secret around Secret Valley is where all the investors’ loot ended up.

That case is still before the courts, which means I can’t really comment.

So to learn a bit more about “land banking”, as it’s known, I called up an old spiv who was up to his neck in it years ago.

He told me that he’d explain how the game worked, on one condition: that he be totally anonymous. Which is totally understandable … especially when you read what he says.

HERE’S his explanation of how land banking works in the get-rich-quick market:

“You buy rural land for $10,000 an acre. You then turn around and market it to investors as a ‘rezoning opportunity’. The sales pitch is that investors could make 10 times their money when it’s developed. The investors think they’re on a winner, and they’ll fight to buy that same acre for $400,000 a pop. All up, you’ve turned a $90,000 investment into $2.4 million.”

So how is it possible to convince people to buy these plots of land?

He explains:

“You need the best salespeople, and the best salespeople are women. There aren’t many of course, but they’re absolutely dynamite. No one thinks a woman will rip you off, right?

“It works like this. They make three calls.

“The first is to deliver a brochure — something elaborate, expensive, and high quality — lots of bullshit.

“The second call is to find out how much money they have. No one wants to waste their time. They’re getting to know the investor, asking about their kids and stuff, but really all they’re doing is drilling down to see if they have any money.

“This is where it’s easy. Most people have access to their retirement funds. That’s the big opportunity … that’s the honeypot! They look upon it as dead money and are willing to gamble with it. They’re a bit more wet behind the ears in Australia — they have this belief that property never goes down.

“The third call is to land the sale. If you have a client who has money, they’ll pull the trigger. However, you don’t just want to sell a piece of field for $10,000 to a guy who has $1 million. You want to flog him more. The technical term is ‘load up the client’. Generally, if they buy once, they’ll buy five times.”

“LOOK,” he continues, “I graduated from doing small time deals. Suddenly I went from having no money in my account to having $750,000 … in three weeks.

“It’s a fool’s paradise, though, because it doesn’t last. It never lasts. You’re earning $200,000 a month, so you buy a fancy car and you fly first class. But then everything catches up with you. The press catches on to it, investors get shirty, and instead of earning $200,000 a month, you’re earning $20,000.

“I didn’t feel good about myself when I was doing it. Of course. I had really low self-esteem. I drank a lot to block out the reality. I didn’t feel worthy, so I got rid of the money as quickly as I could.

“The truth is that I even got scammed myself by another crowd. Overall, I think I turned over $15 million. You’d expect me to have $10 million. I don’t.”

SO how did it end?“

We could have sold more plots if it weren’t for articles in the newspapers. That’s what screwed us up. People would Google stuff and it made our job almost impossible. We ended up closing ourselves down and heading overseas — the writing was on the wall.”

Except it wasn’t.

This old spiv left the game seven years ago. In the meantime, there’s been land banking schemes from Bendigo to Ballarat, from Shepparton to Secret Valley. It’s been reported that, in the past few years, thousands of Aussie investors have sunk more than $100 million — and possibly as much as $300 million — into land banking schemes. Strewth!

So, as I wrap this column up, there’s probably one last question left unanswered:

Aren’t I effectively doing a bit of “land banking” with my farm?

No.

As I type this I’m watching a few grain-fed sheep fertilise my drought-ravaged paddocks. Seriously, there are better investment opportunities going round. But ... it sure is peaceful out here.

Well, most of the time.

Tread Your Own Path!

Are we in a housing bubble?

Are prices going to crash by as much as 50 per cent, as some experts predicted in the news this week? Will the government have the ticker to change the negative gearing rules?

Are prices going to crash by as much as 50 per cent, as some experts predicted in the news this week?

Will the government have the ticker to change the negative gearing rules?Well, to answer these questions, and offer some views on livestock, this week I caught up with none other than the newly crowned Deputy Prime Minister of Australia, Barnaby Joyce.

And in doing so, I worked out we actually have quite a lot in common: we’re both country blokes. We both have a love of numbers. And we both have a habit of saying whatever’s on our minds at the time.

Barefoot: “Thank-you for your time Deputy Prime Minister. I currently own two Alpacas on my farm, and I just don’t care for them at all. They’re more stubborn than Greens Senator Sarah Hanson Young. Have you ever been spat on by an alpaca...or a Greens supporter?”

Barnaby: “No, although I’ve actually had alpacas run alongside me as I go for a jog down the side of my road. They just look like too much…hard work”.

Barefoot: “First home buyers have the footprints of property investors squarely on their backs. Negative gearing has created an uneven playing field because they can write off their losses against their tax. Explain to me how this is fair or productive?”

Barnaby: “Well….there are affordable houses, there just mightn’t be affordable houses in the places you’re looking. When people say there’s no affordable houses, well that’s not correct, there are, and in regional areas they’re vastly more affordable than in the cities”.

“Look I bought a house in St. George in South-West Queensland. I lived out at Charleville, now I’m living south-of Tamworth, but here’s the thing: I’m still out of town where it’s cheaper. What I’m saying is you’ve got to look across the nation. If you look around and say the houses around me are unaffordable you’ve got to ask yourself... is there somewhere else you can go where they are affordable?”.

Barefoot: “So what you’re basically saying is the Government doesn’t have the ticker to touch negative gearing, right?”

Barnaby: “The problem you’re going to have is that if you start messing around in any place without a proper plan, the problems you can create can be vastly greater than the problems you had. If you go into any market and take a substantial group of people out of that market, you can have an incredibly detrimental effect on all the people who have currently bought a house. There’s two sides to every equation”.

Barefoot: “Yes, but there is a substantial group of people who right now are priced out of the housing market. They’re called first home buyers”.

Barnaby: “There are two groups of people who you always have to consider: the people who want to get in and the people who are already there. So it’s never a simple equation, if you’re going to say I’m going to make all houses cheaper, you’ve just made all the people who own houses or owe money to a bank on a house, poorer”.

So here’s my take out from my discussion with the Deputy Prime Minister.

There is absolutely zero chance the government will do anything more than fiddle around the edges of negative gearing policy.

As Barnaby says there are two sides to every equation -- and make no mistake, in politics the side that wins is usually the one with the most voters -- and roughly two-thirds of Australian voters are homeowners.

It makes perfect political sense: who the hell wants to be remembered as the government that pricked the biggest housing bubble in history?

Well, I’ll tell you who: Bill Shorten.

He’s got nothing to lose, so he’s prepared to roll the dice, and end negative gearing for existing homes.It’s bold, and it’s brassy.

But there’s just one little problem with it: getting Aussies off negative gearing, is alike a junkie getting off the gear. Long-term it’s totally the right thing to do. Just not today...maybe tomorrow (but probably not). The scary part is that everyone knows there will be a withdrawal period, and it will be nasty, and no one can accurately predict what will happen. But let's have a go...

Bill Shorten has said that if he’s elected, negative gearing on existing properties will be axed on the 30th June 2017. However, he’s also assured landlords (and his party) that anyone who buys before that, gets grandfathered tax deductions for life.

So, what do you reckon the property market will do in the run up to the cut off date?

Boom, baby!

What will happen the day after?

Will we be shivering in in a corner, with our heads in a bucket?

Who knows?

Either way we should encourage our politicians to make hard, courageous decisions, that benefit the country in the long-term. However the trouble is for a politician, long-term isn’t even a three year electoral cycle these days -- just ask Kevin, (and Julia and Tony).

So where does that leave first home buyers, with the likelihood that the Barnaby and his boys will be returned to power?

Well, last year the former Treasurer, Smoke’n Joe Hockey’s advice to young people who were struggling to crack into the Sydney property market was to ‘get a good job that pays good money’ (teachers, nurses, police-women, scientists... no house for you. Lawyers, bankers, politicians, you win!).

When I asked Barnaby the same question, here’s what he said:“

The great thing about Australia is if you’ve still got the drive, if you’ve still got the mongrel about you that wants to get up and go, you’ll get there. But if you think you’re going to – by some stroke of luck – walk into a multi-million dollar place for a couple hundred thousand bucks, well that just ain’t going to happen. Like everything in life you’ve got to start from the bottom, work hard and you’ll get there”.

Tread Your Own Path!