Articles & Questions

Every week I publish a fun new article on a money topic I think you’ll find interesting. I also answer a handful of reader questions. Subscribers to my newsletter get to see everything first — but you can browse some of my past articles & questions on this page.

My Best Articles

Not sure where to start? Below I’ve handpicked a few of my favourites. And if you like what you see, don’t forget to subscribe to my free newsletter to get new issues before anyone else!

Search Articles

Dating an Orange Narcissist

An old mate of mine turned up to the farm with a baseball cap on.

It wasn’t sunny.

As we shook hands I noticed his head was bandaged.

“What have you done to your head, cobber?” I asked, concerned for his wellbeing.

An old mate of mine turned up to the farm with a baseball cap on.

It wasn’t sunny.

As we shook hands I noticed his head was bandaged.

“What have you done to your head, cobber?” I asked, concerned for his wellbeing.

“I’ve just had a surgical procedure,” he said. “Grafts.”

I had no idea what that meant.

But apparently, a surgeon yanked the hair from his rump then sewed it into his noggin, like a seed. And then my mate spent the next few weeks watering it with enough worm juice so that hopefully a few bum hairs would sprout.

Or something like that.

“How much did this hair-raising procedure cost you?” I asked.

“Forty grand,” he said sheepishly.

“No,” I gasped.

“Yeah, yeah,” he laughed.

Now my mate paid for this out of the savings in his Smile bucket.

But if you're missing both your hair and your savings, help is at hand:

“Thinking about a hair transplant but the cost is holding you back? You may be able to access your superannuation on compassionate grounds to fund your treatment…”

Check this Facebook ad out:

Huh?

In 2024, Australians lodged more than 90,000 applications to raid their super early on compassionate grounds. Over a billion dollars was released, mostly for medical costs. Authorities are now calling out businesses that push people toward overly expensive or unnecessary treatments funded by their retirement savings.

And some of those treatments include hair transplants.

Apparently this now falls under ‘mental health’.

Right.

Getting bum fluff sewn into your head and calling it a mental health necessity is a stretch.

But think about what happens when these blokes are old and grey and finally do the maths. Factor in the tax on early withdrawal and decades of lost compound interest, and that $40,000 procedure can quietly turn into a $200,000 mistake.

All for something that, in most cases, is optional.

My mate can afford it. Plenty of people can’t.

And they’re the ones being sold.

One day they’ll stop working. One day they’ll have to start living off what’s left. And if they’ve been dipping into it early, that moment will arrive with less than they thought.

It’s enough to make you tear your hair out!

Tread Your Own Path!

P.S. We're heading into the school holidays, so I'll catch you in a couple of weeks!

Your Questions & Answers

Dating an Orange Narcissist

Am I Really the Bad Guy?

I Spent $800 on takeout food

Dating an Orange Narcissist

Hi Scott,

A lot of us Barefooters signed up to ING back in the day for the free banking and the good rates. Now I'm reading they've rolled out a paid subscription model overseas, up to $75 a month for the bells and whistles, and Australia's apparently on the list. If ING goes down that road, where are we all supposed to go?

Daniel

Hi Daniel,

I rang up ING (admittedly when I was at the boozer).

"We're not doing it this year," the employee assured me.

So next year then.

After all, the big boss in Europe gave an interview to Bloomberg under the headline: "ING introduces subscription model to lift fee income." It also confirmed our little penal colony was on the list for the gouging.

"He said the quiet bit out loud ... that makes your job hard," I said.

"Uh, yes, it does," he said.

My view?

Banking is a lot like dating a narcissist.

When you first hook up they're all lovey dovey, and low-maintenance:

No bank fees! No ATM fees! High savings rates!

Then they get comfy. And slowly the hoops appear:

"Show me your pay packet if you want a good rate."

"Don't you dare touch your own savings, or my interest in you will... vanish."

They treat you worse every year ... putting out less and less, betting you're too busy to leave.

So where to next?

Well, I had a brief affair with UP, yet they ended up jerking me around as well.

My business banking is with a credit union, but that's kind of like listening to music on a walkman. It's financial virtue signalling, and mostly impractical.

Personally, I'm not playing banking Tinder, swiping right on every outfit that flirts with an extra 0.7%, knowing full well it disappears the second the honeymoon ends.

My view?

ING are not the sweetheart they were when I first wrote my book, but they're no Big Four either.

A subscription fee to hold my money though?

That'll be the day I tell them to pack their bags.

Am I Really the Bad Guy?

Hi Scott,

Both my parents have passed away and I'm inheriting the family home 50/50 with my sister. Neither of us plans to live there. She wants to keep it for sentimental reasons. I want to sell. It's a large acreage with an older house. Mowing, weeds, rodents, the works. And I can't stomach an empty house when people in our community are desperate for somewhere to live. My sister wants to buy me out via a long-term payment plan. But she's already said "you don't really need the money anyway," refused any discussion about terms, and forbidden me from asking about her finances. I've suggested she borrow from a bank instead. She thinks I'm being unreasonable. I'm yet to start a family and this money matters. Why does wanting my fair share make me the bad guy?

Tim

Hey Tim,

Your sister is grieving the loss of your parents, and right now that's guiding her decision to keep the joint.

You also said you're 'about to inherit the home' which tells me it's still pretty raw.

This is what happens mate! It's a totally understandable reaction.

So what can you do?

Give her some time. (You've got two years from the date of death before Capital Gains Tax kicks in.)

The reality of maintaining an acreage property is a pain in the toosh, and expensive as hell. So give it six months.

At the same time I'd find a way to honour your parents and your family. Maybe it's starting a new tradition, a yearly long weekend retreat that the entire family goes on. Or perhaps it's a donation in their name.

My wife's late father was a teacher. Each year she and her brother go back to his old high school and present a prize to a student in his name. It's sentimental, meaningful and hopeful all wrapped up in one night.

Better yet, ask her for some ideas.

You're not the bad guy. You're her brother, and with a little support you can help her with her grief, and help her use the money to honour them. That's the legacy they'd be proud of.

I Spent $800 on takeout food

Scott,

In 2021 a friend recommended your book to me. I was in a bad place, in a relationship that was incredibly abusive, emotionally and financially. I read it that Christmas and went through my spending. I was spending $800 a week on takeout because my cooking was "too shitty" for him to eat. After I'd worked a full day and he'd spent it gaming because "no one is hiring babe."

That was a devastating wake-up call. I restructured my spending and started saving. By the end of 2022 I was free. Tonight I got my end of financial year bonus. I've officially hit my 20% deposit goal, Scott. I can buy a home. I am happy crying right now. I have six months of expenses saved, a healthy ETF account, and I am free.

Sara

Hey Sara,

Hallelujah!

There is so much doom and gloom right now.

The government. Capital gains tax. The cost of living. All very real speed bumps. Yet the algorithm of outrage makes them feel like dead ends.

Not you, Sara.

You were in a genuinely awful situation. A bloke who wouldn't eat your cooking and wouldn't get a job.

Yet instead of staying stuck, you opened a book, set up some buckets, and followed the plan.

Year one you sorted yourself out.

Year two you walked out the door.

Year five you're happy crying over a deposit.

That is its own special kind of compounding.

I've answered thousands of letters over the years. What I've found is it takes most people about 12 months to sort themselves out, and around six years to become financially bulletproof.

Not many people follow a plan for five years. But the ones who do get moments like this.

A home deposit. Six months of expenses in the bank. An investment portfolio ticking away in the background. And something far more valuable than all of them:

Freedom. Well done. Enjoy tonight. You’ve earnt it.

Thanks for reading,

Scott

Why I invested in Elon Musk's SpaceX

I just invested in the most overvalued piece of junk going around:

Elon’s latest trillion-dollar trouser-tickler, SpaceX.

I didn’t have a choice. My index fund bought it for me. Automatically.

I just invested in the most overvalued piece of junk going around:

Elon’s latest trillion-dollar trouser-tickler, SpaceX.

I didn’t have a choice. My index fund bought it for me. Automatically.

Because that’s what index funds do. They buy a tiny slice of the biggest companies, and SpaceX just elbowed its way into the club.

And ... I really don’t care.

Now, you may think old Barefoot has foot fungus.

After all, the media has been warning us of the impending DANGER:

“Elon Musk is about to change everything we know about the world of finance in a move experts say will expose millions of Aussies to a new level of risk.”

“Experts warn we’re entering ‘dangerous, dangerous territory’ as the potential concentration of wealth could impact 17 million Aussies.”

“SpaceX risks leaving index fund investors with heavy losses.”

So. Much. Clickbait.

Honestly, I’m so tired of every bloody article being lipsticked with urgency, fear and stress.

So, calmly, the question you want to know is this:

Am I an idiot for investing in a simple, low-cost index fund that buys SpaceX just because it’s a certain size, without even thinking about how much of a stinker this investment could be?

After all, the company lost almost $US5 billion last year. In the first three months of this year alone, it burned through another $US4.3 billion.

That’s the boring numbers stuff buried at the back of the prospectus that only weirdos like me read.

The cool stuff is all the phallic full-page pictures of rockets, and their ballsy aim of the “establishment of a permanent human colony on Mars with at least one million inhabitants”.

Men are from Mars. Elon is from Uranus.

Now, here’s the bit the headlines forget to mention.

I called Vanguard and asked them what proportion SpaceX would make up of my international index fund.

“We expect it to make up somewhere around 0.06 to 0.08% of the index”, they said.

Let’s put that in perspective.

If you have $1,000 invested in an international index fund, your holding in SpaceX comes to:

60 cents.

Sixty.

Cents.

That’s what all the fuss is about.

Yes, SpaceX looks wildly expensive. Yes, AI is being hyped to the heavens. But my index fund owns more than a thousand companies alongside SpaceX and automatically trims the losers.

You know what I love more than spaceships?

Beating the experts who feed the media these headlines.

The annual SPIVA report scores every active fund manager in Australia against the index. Last year, 74% of them lost to it. Over fifteen years, 87% lost to an index fund. Nearly nine in ten.

The people screaming loudest about the danger of index funds all want the same thing:

Your money. Don’t give it to them.

If SpaceX blows up, I lose sixty cents. I’m comfortable with that trade.

Tread Your Own Path!

Your Questions & Answers

I Live With a Man I No Longer Love

I’m Panicking!

The Latest Barefoot Scam

I Live With a Man I No Longer Love

Hi Scott,

I live with a man I no longer love. I stay because he has an autoimmune disease from a tick bite nine years ago. He hasn’t worked in 12 years. He tried day trading from home, failed, and now runs a fridge magnet business with a mate. He earns less than $18,000 a year. I pay the mortgage, the bills, the food, the clothing, and some of his medication.

He is mean, lazy and rude most of the time. I read your book, set up my accounts, and built real wealth. I’ve got $200k left on the mortgage of a house I bought without him (because he told me property was a bad idea). I have also got well over $1 million in super. He also told me contributing to super was dumb because it locked up my money.

Now a lawyer tells me he could walk away with more than 50% of everything I built. I don’t know what to do. So I stay? I’m 55 years old. Am I really going to walk away with only half of what I created?

Wendy

Hi Wendy,

It sounds like you’ve already made your mind up.

You just haven’t packed your bags and walked out the door, yet.

Now you’re writing to me, a finance guy, asking for permission to leave him.

Well, fair enough:

“You have permission.”

Look, there’s a reason you’re in a strong financial position, and he isn’t:

You did everything right. He sounds like he was a bozo (even before the tick).

Now you’ve seen the family lawyer and it sounds like they have said his ongoing illness and lack of income will be a factor in your separation.

And if that’s the price of financial success, I’d gladly pay it.

Why?

Because there’s honour in having looked after someone who has been a significant person in your life, who can’t fend for himself. That’s hard to accept for sure. But, Wendy, you’ve been doing this for years. At least this draws a line around it.

Yet, most importantly, because that money buys you your freedom.

You have 25 years of good living ahead of you to find someone you do love. You have a good amount in super, a nearly paid off home, and enough saved to spend six weeks in Europe with your friends. It’s not like you’ll be starting over. I’d call that a hell of a head start.

Tick. Tick. Tick.

I’m Panicking!

Hi Scott,

I’m a single mum to my 13-year-old son. After years of struggling, I found your book, followed the steps, saved a $50,000 deposit – and have just finally landed a great new job earning $119,000 a year. I got pre-approved last week and had an offer accepted on a $700,000 freestanding house. But when I stared down the barrel of the $4,200 monthly repayments I panicked. It left almost nothing to actually live on. So, I called the agent and pulled my offer. I’ve now set a hard ceiling of $650,000 to drop my repayments to $3,700 a month, which feels safer. Here’s my dilemma: The market is softening slightly, but I’m terrified of my deposit just sitting there. Do I keep hunting for a cheaper house, or do I rent for another year and keep saving?

Rina

Hi Rina,

I’m sitting here on the farm reading your question when a Luke Combs song came on. Growin’ Up and Gettin’ Old.

The killer line: “I ain’t lost a step, I just look before I take ’em."

That’s you. That’s exactly what you just did. You’re a smart, successful single mother who values safety and security for her son more than being talked into a transaction by a mortgage broker and a real estate agent chasing their commissions.

My advice?

Keep renting. Keep saving. And keep looking. The right place will come up soon enough.

And when it does, you’ll know.

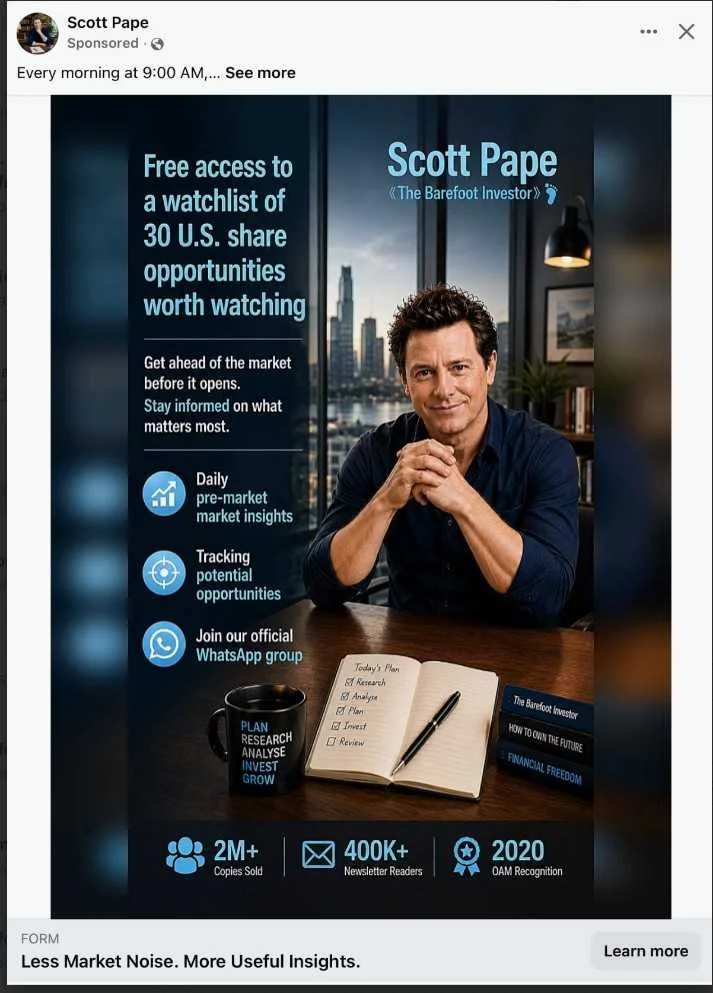

The Latest Barefoot Scam

Hi Scott

A post from you popped up on my Facebook, with an offer of seeing your watchlist of US shares to buy.

I’ll admit I was taken in by it, especially that the poster was “Scott Pape”. It does look very professional, and even mentions your Order Of Australia medal! However, it involved going into a WhatsApp group, which is obviously a scam. Just thought I’d let you know.

Bruce

Hey Bruce,

Yes, it’s a scam.

(My barber Benny is absolutely furious at how the scammers have depicted my hair. My personal trainer Shane, however, is very pleased with the forearms.)

The scammers are using AI to churn out hundreds of these ads, reposting them faster than I can round them up while sitting at the farm swearing at my sheepdog Lucky.

So here’s the tip:

Social media profits from these ads. So I quit posting on socials entirely.

If you see a post from me, know this:

It’s not me.

Thanks for reading.

Scott.

Barefoot’s Take on the Budget

A spinner from the Housing Minister’s office called me a couple of weeks ago:

“The Minister would like to invite you to Canberra to attend the Budget. There are a few changes we’re going to announce that, let’s just say … we think you’ll be very interested in”, he purred.

“Yeah, yeah. You blokes always say that. What’s the date again?” I asked, turning off my tractor.

A spinner from the Housing Minister’s office called me a couple of weeks ago:

“The Minister would like to invite you to Canberra to attend the Budget. There are a few changes we’re going to announce that, let’s just say … we think you’ll be very interested in”, he purred.

“Yeah, yeah. You blokes always say that. What’s the date again?” I asked, turning off my tractor.

“It’s the 12th of May”, he confirmed.

I pulled up my calendar.

On the 12th of May I had one all-day event scheduled:

“Colonoscopy.”

Yes, I’d booked an anal probe, completely forgetting my other Canberra clean-out with Dr Jim Chalmers.

Seriously, this column writes itself. (It would be funny if I wasn't completely TERRIFIED.)

It gets better though. As I lay on the cold operating table on Tuesday, my backside blowing in the breeze, the anaesthetist appeared hovering over my head:

“I just want to say I’m a huge Barefooter. Your book changed my life. You took some time off the column, but I’m glad you’re back. Now go to sleep … deep sleep …”

Meanwhile in Canberra, as a nation we collectively clutched our coits as Dr Jim pulled on his rubber gloves.

The changes to negative gearing and capital gains will make property investing less attractive. I’m happy to cop that if it takes a bit of heat out of house prices. My kids need somewhere to live one day. So do yours.

He also tightened the squirrel grip on trusts and capital gains tax. But you’ve already read a thousand boring headlines about all this since Tuesday so I won’t go on.

Yet here’s what I actually think mattered:

The Government did not touch the two tax-free foundations of the Barefoot Steps: your family home and your super. In other words, even though some rules changed on Tuesday, the Barefoot plan did not.

Finally, I know this is a lot. But if you’ve been sitting on the fence about calling your doctor and getting a full ‘Barnaby Joyce’, just make the call. Book it in. It’s the same rule as investing: the best time to pull the trigger is when you’re terrified.

Tread Your Own Path!

Your Questions & Answers

Albo Buried This on Budget Day – Let’s Dig It Up

We Are Going Under …

Against All Odds

Albo Buried This on Budget Day – Let’s Dig It Up

So I didn't make it to Canberra this week. Yet it turns out that Albo and I had something in common this week: we were both busy burying things somewhere the sun don’t shine. So, for the first time ever, I'm flipping the script — I’m not answering the first question, I'm asking it!

Dear Anthony,

All the headlines this week are asking whether you lied about negative gearing. I don’t care. You saw an opportunity and you took it. Good on you.

Here’s my question: why couldn’t you be bold when it came to our kids?

Australians are the world’s biggest gambling losers – forty percent worse than the country that comes second. That doesn’t happen by accident. It requires fresh-faced kids. And over a third of 12- to 17-year-olds are already gambling. Gamblers Anonymous is now seeing teenagers at its meetings.

The late Labor MP Peta Murphy handed you 31 recommendations, and her dying wish was urgent reform. You had bipartisan support. You sat on it for 1,050 days. Then, while every journalist in the country was buried in the budget lockup and I had a camera up my clacker, you quietly slipped it out.

Now, you could have gone on The Today Show and said:

“These companies have hijacked our sport and they’re targeting our kids. I’m banning the ads.”

(And I think every parent in the country would have fist-pumped their Weet-Bix off the table, even the ones who love a punt.)

But you didn’t.

Is it any wonder voters are done with the party machine? You’re the most powerful man in the country, Anthony. You just proved you can be bold when you want to be.

So why not for the kids?

Scott

We Are Going Under …

Dear Scott,

My husband and I are both 53, earning $120,000 each. Our 18-year-old is at uni and still lives with us. We have two younger boys (16 and 14) with ADHD, both on medication, both seeing specialists, and studying with tutors because they have difficulties at school. The medical bills are brutal.

We owe $35,500 in unpaid school fees and carry a $1.25 million mortgage. Fifty percent of our income goes to the mortgage alone. Some months we spend more than we earn. On top of that, both my husband and I have some pretty serious medical issues – and yet we’ve been skipping seeing specialists for fear of even higher bills. My husband took a new job to earn more money, but he’s not sure it will last. The tension at home is constant. We yell at each other about cheese.

We’ve seen a financial counsellor, who told us nothing new. We have tried the Barefoot buckets but there is not 10% left to put in any bucket. We don’t know whether to sell the house, rent it out, hold on, or let go. Scott, we are drowning. Please guide us.

Maria

Hi Maria,

I want to share something with you.

Many years ago, at a deserted beach, I got caught in a rip.

It happened so gradually I didn’t notice at first. I thought I was in control. Then I realised I was moving steadily out to sea.

At first, I panicked. I screamed and waved at the lone surfer on the shore. I stripped off my clothes, thinking it would help me stay afloat. It did. But only for a minute.

Then I got so tired I remember thinking I couldn’t go on. That I’d just let the waves take me.

That’s where you are right now, Maria. There are no boats coming. No one else can make this call. But if you're asking me what I'd do in your situation, here's the lifejacket:

Sell the house. Rent. Demolish the debt. Regroup.

You couldn’t afford it even if every one of you was in perfect health. But you’re not. Every person under your roof needs medical treatment, counselling, or extra tuition. These are needs, not wants.

And the private school? You’re paying overdue fees and private tutors. If they can’t get your kids across the line without backup, what are you actually paying for?

One rate rise, one car noise, one bad day at the new job, and you get sucked under and don’t come back up. You’re skipping seeing specialists for fear of bills. That terrifies me more than the mortgage.

Right now you have choices. That won’t always be true.

Reach out and grab the lifejacket, Maria.

Before the rip takes you.

Against All Odds

Hi Scott,

I’m a 25-year-old woman looking for help with my super. I was kicked out of home when I was 16, and due to this I have no parental figures to ask for guidance. After all that trauma, I’ve finally got to a place where I’m financially stable (mainly thanks to your book, The Barefoot Investor, which has been a godsend). I’m now looking to set myself up for retirement. I’m wanting to know what’s the limit to insurance on my super fund. How much in weekly fees for insurance is too much? I’ve got just under $30,000 in my super fund. I work a blue-collar job (parts and accessory fitter). I’m unsure what cover I need and what fees I should settle for. Please help, and thank you.

Sarah

Hey Sarah,

It sounds like the trauma you faced as a kid has defined you, in a good way. You want security, and from the questions you’re asking I have absolutely no doubt you’ll never be financially vulnerable again.

You are a winner.

Now, to your question:

Blowing out 25 candles kickstarts your super fund charging you for default insurance cover.

Is it worth it?

Bloody oath. Default insurance super starts off pretty cheap, around $300 a year for a combined policy that covers you for dying, being left totally disabled, or losing your income if you need extended time off work.

Of course, without kids or dependants you don’t have to worry too much about dying … it’s the cover for being ‘nearly dead’ (disability, loss of income) that’s important for you.

You got this.

Thanks for reading.

Scott.

Are you okay?

“Don’t make me stop this car!” I roared at the kids in the back. And then, for possibly the first time ever, I actually followed through.

I stopped the car. The kids froze.

I took a long breath, looked out the window, and noticed a half-boarded-up pizza joint.

“Let's get some pizza”, I said.

Inside, it was empty. No phones ringing. No music. Just a tired woman behind the counter with tattooed-on eyebrows, staring straight through me.

“One family-sized Margherita, please."

We sat at faux-wood tables while I flicked through a Woman’s Day magazine:

From October 1987.

The headlines were perfect:

“Take 2 inches off your hips in 2 weeks.”

“Which makeup colours make you prettier?”

“AIDS HYSTERIA: How much fear makes sense?”

Every second page was an ad for ciggies, or pictures of women in leotards smoking Alpine menthols.

The magazine smelled like the vinyl backseat of our old Ford Falcon. Warm. Faded. Casually sexist.

This week, an ANU study found nearly three in five Australians believe that life was better 50 years ago … and I was holding their evidence.

Okay, so let’s not pretend 1987 was all apricot chicken. HIV/AIDS was coming for everyone. The devil had slipped secret messages into AC/DC songs (if you played them backwards), and kids risked getting square eyes watching too much Scott and Charlene (ask your parents).

Yet flicking through those musty pages I was struck that there was nothing on side hustles, investment properties, or the hand-wringing of how your kids will ever afford a home.

Makes sense.

Back then a house cost about three times the average income. A family home was something you worked towards, and paid off – then set your sights on a shiny new Commodore.

Yet just as that magazine was hitting the printing presses … everything changed.

The share market crashed.

Interest rates rocketed to 17%. The economy did the Locomotion. Finance hit the front pages, and never left.

And then? Well, then came the biggest borrowing binge in history … and it’s still going strong 40 years on.

Houses now cost a staggering ten times the average income.

Every year we borrow more, we stress more, and we lie awake wondering how our kids will ever afford something as basic as a roof over their heads.

On paper we’re wealthier. But we’ve never been in more debt, or more stressed and depressed.

The pizza came. It was horrific. The kids looked at me. I looked at them, and said: “You get what you get and you don’t get upset.”

They had no choice but to eat what they were served. That’s how life works!

Tread Your Own Path!

Your Questions & Answers

My Husband’s $100,000 Gambling Debts

Is HESTA Super Going Broke?

Welfare Check: Are You Okay, Barefoot?

My Husband’s $100,000 Gambling Debts

Hi Scott,

Over the last four years I have paid nearly $100,000 dollars of my husband’s gambling debts. He still has $55,000 dollars to pay on a personal loan, and he says he needs $6,000 immediately to tide him over. He refuses to show me evidence of his transactions – I suspect he owes more than he is telling me. My salary goes into the offset account but he keeps his account separate. If I don’t pay his debts, he stops paying for groceries and stops contributing to the mortgage. I turn 50 this year. I am afraid for my emotional and financial wellbeing, and for that of our son. However, I don’t have the family or social support to separate immediately. I am trying to get my head around this situation without losing myself. I need to protect myself and my son financially while I work out what to do. I would really appreciate your help.

Sally

Hi Sally,

You must be absolutely exhausted.

Here’s the brutal truth: this isn’t over. It won’t stop until he puts his hand up and gets help. And even then it’s a long, hard road back through the financial wreckage this has caused.

You are dealing with a disease that is designed to take every cent it can get its hands on. I see the damage it causes every day.

My advice?

It’s time to be ruthless. For your son.

Do not pay another dollar towards your husband’s gambling debts.

Do not give him any money. Pay the bills yourself.

As long as you keep covering for him, this will continue.

Then, make two appointments. First, call a financial counsellor (National Debt Helpline: 1800 007 007) and get a plan in place to protect yourself. Second, see a family lawyer so you can understand your options.

Hope is not a strategy. You’ve carried this for four years. That has to stop. And it starts by getting the right people around you. Reach out to me this week, and I’ll help.

Is HESTA Super Going Broke?

Hi Scott,

I’m so mad at my super fund, HESTA, right now. I’m 44 and I’ve been with them for years. I have $250k with them, but I’m ready to jump ship after recent reports that their administrator (Grow Inc) has significant debt. Not to mention the argy-bargy HESTA put a lot of members through when they switched to said administrator last year.

I have no trust in their ability to safeguard and invest my super anymore. But I also found out that Vanguard Super also uses the same administrator, so I’m nervous about moving my funds just to land in the same pot of trouble. Am I being too hasty? Or has HESTA bollocksed it up enough to warrant a move?

Cheers,

Sash

Hi Sash,

Your money in HESTA is safe.

However, I’ll leave it to you to decide whether you want to put up with their half-arsed service (and why Vanguard recently decided to YOLO with Grow).

Could you imagine if CommBank came out and said:

“In an effort to save us a bit of dough, we outsourced our entire customer administration process to a dinky little outfit … and it appears they’ve stuffed things up. So you won’t be able to access your bank accounts for the next seven weeks. Starting now.”

They’d be taco meat by Tuesday.

Well, that’s effectively what HESTA said (and did) last year!

My view?

Super funds have got their outsourcing completely arsed about:

They spend thousands of millions each year flying around the world first class trying (and failing) to pick winning investments. (This despite the fact that the evidence is unequivocal: they should outsource their investment decisions to a low-cost index, and return those thousands of millions of dollars to our accounts).

Yet they have outsourced the very thing that their customers need: reliable, safe and seamless access to their money! This explains why rolling over your super fund is harder than getting a council permit to build a shed.

It’s a total disgrace.

Welfare Check: Are You Okay, Barefoot?

Hey Scott, just wanted to check in. Haven't seen any newsletters or articles in the Herald Sun lately. RUOK? Missing your wise words.

Deb

Hi Deb,

Thank you for checking in ... and to the many readers who wrote asking the same thing.

I can confirm I am okay!

I've been writing this column for 23 years. When my first son was born, I asked my editors if I could take school holidays off to spend time with him. They reluctantly said yes.

Twelve years on, I'm still holding that boundary. In fact, it's even more important to me today. After all, I only have six more years with him at home.

That's wealth to me.

Thank you for reading.

Scott.

Shiver Me Timbers

Hi Scott,

I have a friend who offered to manage my superannuation for me.

Hi Scott,

I have a friend who offered to manage my superannuation for me. So I transferred all $173,000 from Australian Super to his SMSF. Long story short, he started trading with an overseas firm (Swipe Capital) and it was a scam. It’s all gone, plus around $50,000 of my savings I put in too. I’m really angry with my ‘friend’ who I thought knew what he was doing but traded with an unregulated company overseas. All my Google searches about this company say the same thing: ‘red flag’ or ‘scam alert’. Where do I stand in regard to the $223,000 I’ve lost – can the government do anything, or is it gone forever?

Lincoln

Lincoln,

Your super was with the equivalent of a Sydney ferry, large, boring, and packed with the public – and your mate stowed you both on board a pirate ship, with Captain Feathersword at the wheel. Shiver me timbers!

Your mate walked you off the plank, but you do need to take some responsibility here, mate. You handed control of your super to a friend, and that’s where you got peg-legged. Aghh!

You could speak to a lawyer about whether your friend breached his duties as a trustee. But if he’s been looted too, then chasing him may cost more than you’ll ever recover. So by all means report it to ASIC and SCAMwatch, but do it knowing there’s a very good chance the money is gone.

They’ve stolen your money. Don’t let them take everything else with it. People who get scammed lose more than money. They lose their confidence, their peace of mind, and sometimes their will to keep going. Call IDCARE on 1800 595 160. Talk to someone who gets it.

Guard your mental health like treasure.

The Iran War is Killing My Retirement

Hi Scott,

I am very stressed about the Iran war, and the impact it will have on my superannuation. I am 61, still working, and looking to retire in the next four years.

Hi Scott,

I am very stressed about the Iran war, and the impact it will have on my superannuation. I am 61, still working, and looking to retire in the next four years. Therefore I check my Australiansuper balance if not daily, every second day! I spent the last 60 years not giving a cuckoo about the share market, and now it keeps me up at night. Experts are suggesting that this is the start of something much bigger. I am thinking of moving my super to cash until this blows over. It would help me sleep at night.

Yasmine

Hi Yasmine,

You wrote: "I spent the last 60 years not giving a cuckoo about the share market."

That might actually be the smartest investing strategy I've ever heard.

Because when retirement is four years away, every wobble in the market suddenly feels personal. It's like waking up an hour before your alarm. Every creak in the house suddenly sounds like a burglar.

On Monday, as I was sipping my coffee, I read this headline:

"More than $100 billion was wiped off the ASX in less than an hour in a horror morning for Australian investors."

I actually love these headlines, because they are just so… thirsty.

Let's decode it:

"$100 billion wiped off" (seems like a lot)

"in less than an hour" (seems quick)

So was it a horror morning for Australian investors?

Nah.

Another way of writing that headline is:

"Sharemarket down to levels not seen since… Christmas."

Even accounting for Iran and the $100 billion wipe out, over the last year the sharemarket has delivered a 14% return, when you factor in dividends (which you should).

Ho! Ho! Ho!

So I have some advice for you to get more sleep.

First, stop checking your super balance every week. It's like planting an apple tree … and then checking on it each morning and wondering whether you should pull it out and replant it somewhere sunnier in your garden.

Second, build up a cash buffer within your super fund. Money you can live off when you retire. Book in to see a financial adviser at AustralianSuper.

Something like three years of living expenses is a good number.

Sleep well.

Have You Checked Your Super Lately?

Hi Scott,

I read your column about Mary (“I’m Still Standing”), who lost the majority of her lifetime super savings through the First Guardian Master Fund collapse.

Hi Scott,

I read your column about Mary (“I’m Still Standing”), who lost the majority of her lifetime super savings through the First Guardian Master Fund collapse.

I’m the government-appointed CEO of the Compensation Scheme of Last Resort.

Around 12,000 people were impacted by Shield and First Guardian, but only 2,000 have lodged complaints with the Australian Financial Complaints Authority (AFCA). What happened to the other 10,000?

If you received dodgy advice, you may be eligible for compensation. Lodge a complaint with AFCA. And encourage everyone to check their super balance now! Love your work. Keep giving the bad guys a hard time.

David Berry, CEO, Compensation Scheme of Last Resort

Hi David,

Your job is to compensate Aussies who have received dodgy financial advice?

Bloody hell, you’d be busier than TAL’s funeral insurance public relations team.

Here’s my best guess on where those 10,000 missing victims are:

They have no idea it happened.

The vast majority of people who got screwed innocently clicked on a Facebook ad offering a free super comparison or review. They were taken to a page that asked for their phone number. Then a smooth-talking spiv convinced them to move their super into a dog-turd super fund.

Then their money went ‘poof’!

And here’s the thing about super: it’s the one account we never check. It just sits there while we get on with life. Which is exactly what these crooks were counting on.

So let’s give a brother a hand.

There are a couple of million Barefooters reading these words right now.

So I have a favour to ask of you.

If you, or someone you love, ever clicked on a social media ad and switched your super, or if a financial advisor has switched you into a super fund, go here right now to find out if you’re affected:

Jeffrey Epstein and Vanguard

Scott,

As a mid-life woman, I have been impacted by predatory behaviour in the workplace and I identify strongly with the women who were treated as prey in Epstein’s network.

Scott,

As a mid-life woman, I have been impacted by predatory behaviour in the workplace and I identify strongly with the women who were treated as prey in Epstein’s network. I am really disturbed to read about the links of this network to Vanguard. Are you able to recommend some alternative low-cost ETFs that are more ethical about how they do business, like Future Group, which holds Future Super?

Matilda

Hi Matilda,

Your question made me sweat like Bill Gates.

Jeffrey Epstein is linked to Vanguard?

I couldn’t believe it. This is one of the most boring companies in finance. Its founder, Jack Bogle, was so tight he kept a penny jar by the photocopier.

He must be rolling in his grave right now.

So I took a deep breath, held my nose and googled.

Nothing.

I asked ChatGPT.

Nothing.

So I called Vanguard and asked them point blank.

“Is it true you have links to Jeffrey Epstein?”

“I don’t think so”, came the confused response. “Have you heard otherwise?”

“Well, I got a tip-off from a reader who’d obviously done some serious research ... though it doesn’t appear to be on the internet, or in any newspapers, or anywhere else that I could find.”

And as I said that, I realised something.

Research isn’t really your thing, is it Matilda?

Because if it were, you would have also googled the ‘ethical’ alternative you recommended to me, Future Super.

Here’s what I found when I did:

It seems Future Super has its own problems: greenwashing allegations, high fees – and ASIC fined them for misleading marketing in 2023. So your ‘ethical’ alternative has about as much credibility as Elon Musk’s email to Epstein on Christmas morning asking for an invite to one of his parties (google it).

Matilda, the whole Epstein tragedy is about innocent young women giving their trust to people who hadn’t earned it, and didn’t deserve it. Don’t make the same mistake with your money.

I’m Still Standing

Dear Scott,

I’m writing to you because I need a little hope.

Dear Scott,

I’m writing to you because I need a little hope.

I’m 56 years old, single, and the sole supporter of myself. I have worked two to three jobs at a time all of my adult life, always believing that if I worked hard and did the right thing then my superannuation would be there to support me in later years.

Unfortunately, due to the failure of the First Guardian Master Fund, I have lost the majority of my lifetime superannuation savings. I now have approximately $13,000 remaining in super, and I am extremely concerned about my financial wellbeing as I approach retirement age with no partner, no safety net, and no ability to rely on anyone else.

I am not looking for sympathy, I’m looking for practical, realistic advice. I want to know what is still possible at my age. Whether rebuilding some level of super is achievable, what the smartest use of my limited income might be, and how to protect myself from making any further mistakes.

I have always been responsible, hardworking, and willing to do what it takes. I just feel overwhelmed and unsure where to start now, particularly after such a devastating loss late in life. Your work has helped so many Australians feel less ashamed and more empowered about money, and that is why I felt brave enough to reach out. Even a small amount of guidance or direction would mean more than I can properly express.

Mary

Mary,

You are a rolled-gold winner.

You have every reason to play the victim. Your retirement savings are gone. Yet you’re writing to me about hope?

That tells me everything I need to know about you.

However, hope isn’t a strategy.

We attack.

First: I’m putting you in touch with a lawyer already across this issue. If there’s money to be clawed back, we claw it back.

Second: you’ve got roughly ten working years left.

Here’s the rebuild:

Move your super to a low-cost industry fund or Vanguard super index fund. Salary sacrifice like your retirement depends on it. Take advantage of the ‘free money’ co-contribution scheme. Keep fees tiny.

Boring and relentless is where the magic happens.

And understand this: retirement isn’t a cliff. It’s a gradual slope. Part-time work. Flexible income. Super plus the Age Pension. That combination works.

You are not starting from zero.

You are starting with grit, discipline and ten more years of earning power.

That’s enough.

Now go build it.

What’s the Catch?

Hi Scott,

Long time reader, first time writer! After comparing super funds I was contacted by Sue from (FINANCIAL PLANNING FIRM’S NAME DELETED BY BAREFOOT’S LAWYERS)

Hi Scott,

Long time reader, first time writer! After comparing super funds I was contacted by Sue from (FINANCIAL PLANNING FIRM’S NAME DELETED BY BAREFOOT’S LAWYERS) and after answering a lot of questions they’ve suggested I move my $70k Rest super (growth index) to an AMP super where they say they can manage it and improve my return from 9% (500k retirement) to approx 15% (1M+ retirement) due to the larger variety of investing options. The only catch is a one off transfer fee of $3,300 and I’m certain they mentioned another fee of about 1.65% which I believe was recurring. What do you think?

Barry

Barry,

No. No. No.

Barry, just … no.

We are not doing this. Not on my watch. You haven’t been reading me for this many years to get screwed by some cocker spaniel cold caller.

They are lying to you.

The catch isn’t just the $3,300 one off fee. That’s gerbil feed in the scheme of things.

The real snatch is that they are TRIPLING your annual fees. That will end up costing you hundreds of thousands of dollars over your working life.

From your super account to Sue’s savings account.

Barry, stick with your low cost industry fund.

If you want to boost your returns, cut your fees. You could consider moving your current investment option to high growth index funds.

Don’t take the call, make the call: to your super fund.

Scott

Don’t Make Me Google

Hi Scott,

I was recently contacted by an investment company called Caprion Group, which operates in the UK, Australia and New Zealand. Caprion’s account manager is encouraging me to invest $20,000, claiming they only risk 1% per trade and that most trades are profitable. I’m unsure whether this is legitimate or wise.

Hi Scott,

I was recently contacted by an investment company called Caprion Group, which operates in the UK, Australia and New Zealand. Caprion’s account manager is encouraging me to invest $20,000, claiming they only risk 1% per trade and that most trades are profitable. I’m unsure whether this is legitimate or wise. I’m a retired woman living on a government pension, with HESTA as my super fund. With recent market volatility, my super has dropped significantly. On top of that, I’ve just discovered HESTA has frozen all transactions until early June, with no clear explanation. Should I leave my super where it is, and can you tell me if Caprion Group is trustworthy?Jenny

Hi Jenny,

Your question reminds me of a discussion I had with my son just this morning.

“Hurry up! We’ve got to go to your game. Why don’t you have your footy guernsey on?”

“I can’t find it”, he whined.

“Have you looked in your cupboard?” I asked.

“Yeah …”, he said unconvincingly.

I gave him my ‘dad’ stare.

“Oh … kay, I’ll have another look”, he humpfed.

A minute later he came back with it on.

Now, to your question.

First, I googled “Caprion Group + Scam”.

The very first listing was the ASIC MoneySmart website under their ‘investment scam alert’ list.

Their advice? “If it’s on the list, don’t take the risk.”

Jenny, Caprion was on the list.

Next, I googled “HESTA frozen transactions”, and hundreds of articles appeared.

The first article read: “Members of HESTA will be unable to access most services until June, as the superannuation fund undertakes a planned outage to change its administration provider.”

Jenny, as a member of HESTA there’s no need to worry (you’ve only lost access for a while, not your money.) However, if I were the CEO of HESTA, I’d be very worried. The fact that one of the biggest super funds in the country could screw this up so badly is totally unacceptable.Scott

Should I Switch to Vanguard Super?

Hi Scott,

A while back you wrote about Vanguard Super’s upcoming entry onto the Australian scene. I was hoping you could share your thoughts on their performance so far.

Hi Scott,

A while back you wrote about Vanguard Super’s upcoming entry onto the Australian scene. I was hoping you could share your thoughts on their performance so far. All the comparison websites are unable to give more than one year’s worth of data, but that one year is looking pretty impressive, and combined with the low fees it’s hard to ignore. Is this enough information to confidently make the switch?

Linda

Hi Linda,

I’ll be honest, when Vanguard Super launched back in November 2022, I considered switching. After all, I was sure the revolution had arrived: finally someone was going to kick down the door of the $30-billion-a-year super fee racket!

Unfortunately, it’s been less ‘bust the door down’ and more a polite ‘tappity tap tap’: “Oh, excuse me … mind if we join in?”

You see, the truth is that most big funds – AustralianSuper, Hostplus, Cbus, etc – are still partying like it’s 1999: one-size-fits-all aggressive portfolios, bloated fees, and active management that’s basically professional dart-throwing which ultimately leads to much lower returns than index funds over the long term.

The big funds ignore this, because admitting it would mean firing most of their investment manager mates, cancelling the ‘research’ trips to Switzerland, and actually competing on fees. And where’s the fun in that?!

Yet here’s where Vanguard falls down: the fees. It charges 0.58%.

Low? Sure.

Lowest? Not even close.

Ironically, you can get cheaper index options from the same big funds that Vanguard set out to disrupt.

But I’ll let you into a secret: most of the big funds don’t promote their index offerings. Instead, they make you go digging through their investment menus like you’re ordering off the secret Macca’s menu. My guess is they only added them to stop their smart investors jumping ship to Vanguard.

So, yes, I like Vanguard. I own their ETFs. But I haven’t switched my super, because I can get the same index exposure, for less, from the dinosaurs they were meant to replace.

Scott

Should I Go to Cash?

I’m sure you'll get a million questions to this effect, but what should we do with our super based on Warren Buffett’s indicator? Do we move our super investments to more conservative options (cash, etc)?

Hi Scott,

Love your emails!

I’m sure you'll get a million questions to this effect, but what should we do with our super based on Warren Buffett’s indicator? Do we move our super investments to more conservative options (cash, etc)?

Hayley

Hi Hayley

I can’t tell you what you should do, but I can tell you what I’m doing:

Nothing.

Here’s the problem with converting to cash ahead of a crash:

You have to be right twice.

As in, you not only have to pick the right time to sell your shares and move to cash … but you have to pick the right time to buy in again, just before the market recovers.

And, as my wife will tell you, I’m rarely right once … let alone twice!

When you look at the long-term track record of the markets, things have turned out exceedingly well if you follow another piece of advice from Buffett:

“The trick is, when there is nothing to do, do nothing.”

And that’s good enough for me!

-Scott.

Is My Super Genocidal?

Own up, Barefoot, you support the war machine. I have often wondered why my super investments in a fund like Australian Ethical have not grown as much as others.

Own up, Barefoot, you support the war machine. I have often wondered why my super investments in a fund like Australian Ethical have not grown as much as others. It’s because people like you (who I respect) tell them to invest in the fund that will make the most money, rather than the fund that will be best for us as people on this planet. Vanguard enables genocide, mate. Find a well-performing alternate super fund that doesn’t decimate entire populations.

Sandra

Hi Sandra,

I presume you are referencing a report from 2017 where activist investors wanted Vanguard (and other index funds) to dump their shares in PetroChina, Asia’s largest oil and gas provider, because of accusations of genocide.

Vanguard’s MSCI Index International Shares fund contains 1,439 companies (Apple, Nike, Netflix, etc), yet as of today it does not own shares in PetroChina.But it does raise a good point: an index fund simply owns the largest businesses – it doesn’t put an ethical lens on them.

It’s the investment equivalent of a sausage: when you’re at Bunnings on the weekend you don’t ask if the snags are beef, pork or sawdust, right? (“You get what you get and you don’t get upset”, say my kids, who love a bit of sawdust on a Saturday.)

So the solution is ethical investing, right?

Well, that’s like buying an expensive free-range chipotle instead of the humble snag … but you still need to know what goes into it.

Case in point:

AustralianSuper’s ‘Socially Aware’ investment option was found to have money invested in the coal, oil and gas industries, and to own shares involved in nuclear weapons.

Mercer claimed its ethical fund didn’t invest in booze or gambling companies, though it was holding shares in Heineken and Crown Resorts.

Thankfully the regulator is trying to enforce the claims made by fund managers: last month Vanguard copped a record multimillion-dollar fine for misleading investors about the green cred of its own ethical funds.

Enjoy the sausage sizzle!

Scott.

I don’t want this to happen to you

The stock market is flirting with all-time-record highs …

… and that’s my cue to cock my leg and pee all over your portfolio.

You see, I still have PTSD from the GFC, when retirees would write to me in tears as they watched their super balance crater. They had no idea how much risk they were taking in their super fund ... until it was too late.

The stock market is flirting with all-time-record highs …

… and that’s my cue to cock my leg and pee all over your portfolio.

You see, I still have PTSD from the GFC, when retirees would write to me in tears as they watched their super balance crater. They had no idea how much risk they were taking in their super fund ... until it was too late.

I don’t want that to happen to you.

Here’s the problem: while the best-performing super funds label their default flagship funds as ‘balanced’ options, the reality is that they’re often quite unbalanced. They have a large portion of their funds devoted to shares and other growth investments … which juices their returns and helps them win awards.

In other words, if your super fund is consistently one of the top performers, it’s likely they’re taking more risks than the funds they’re competing against.

Now, taking on more risk is great for an 18-year-old dish pig with 50 years of work ahead of him, but it’s potentially disastrous for a 63-year-old executive chef who’s about to light the flame on his last flambé.

Bottom line: Australia’s biggest super funds use an aggressive ‘one-size-fits-all’ strategy which might not work if you’re nearing retirement.

Yet there is an alternative. They’re called ‘target-date funds’ (or ‘lifestyle funds,’ same thing), and they’re becoming more popular, with a large amount of funds offering one.

Here’s the gist:

You pick a target date fund based on your age, and it automatically adjusts your investments as you approach retirement. So, when you’re younger, it invests heavily into growth investments like shares (because you have plenty of time to ride out the ups and downs). As you age, it gradually shifts you into more conservative stuff, like cash and fixed interest.

These funds are a great hands-off option, especially if they’re built with ultra-low-cost index funds.

My advice?

Call your super fund and speak to one of their financial advisors (your first appointment should be fee-free and obligation-free). Ask them to review the asset mix you’re invested in, and have them compare it to the asset mix of an index target-date super fund for your age. Then ask them what they’d recommend, and why.

Tread Your Own Path!

Best Returning Super Funds

I was reading about the best performing super funds, which were Mine Super, Colonial FirstChoice, and IOOF – all of which earned over 10% and easily beat my super fund (AustralianSuper).

Hey Scott,

I was reading about the best performing super funds, which were Mine Super, Colonial FirstChoice, and IOOF – all of which earned over 10% and easily beat my super fund (AustralianSuper). Have you looked at these super funds in detail, and would you consider switching if you were me?

Russell

Hi Russell

I view annual super fund returns tables like I do a tacky beauty pageant:

Fake tans. Fake nails. And the winning fund managers strutting around in evening dresses, posing for investors. Pass me the vomit bag!

The truth is that you do not want to be in the latest ‘hot’ fund.

Why?

Because statistics show that the lucky fund this year is just as likely to be next year’s dog.

Standard and Poor’s looked at the top-performing share fund managers two years ago and found that only 2% of them remained top performers today.

That explains why, over the past five years, 95% of Aussie share fund managers have underperformed an equivalent index fund ETF, after fees.

That’s why I think we should rejig the current super fund table – and instead rank them on fees. Any super fund charging its members over 1% should be made to get in a bikini and parade down Martin Place.

Scott.

What you’re about to read is going to get me into trouble

What you’re about to read is going to get me into trouble.

So I’m going to cut to the chase: to all the marketing managers of the products I’m about to mention, please email my assistant: idontcare@barefootinvestor.com

What you’re about to read is going to get me into trouble.

So I’m going to cut to the chase: to all the marketing managers of the products I’m about to mention, please email my assistant: idontcare@barefootinvestor.com

When I was a kid, I used to try and hide my school report from my parents, hoping they’d simply forget (this was in the days before email, and helicopter parenting).

Yet my plan was always foiled by my older sister, who was the dux of her class, and waited in anticipation all year for her brief bath in the parental sunshine.

Mole.

Well, the Government just released a (long, confusing, boring) report card on your super fund card - it’s called the APRA External Report (www.apra.gov.au), and the worst super funds are hoping that you never read the report.

So let’s dig in.

OnePath was like my Year 8 report card: a total and utter sh…earing show (as my father would say). OnePath was singled out by the regulator for having no less than 33 dud super funds.

Thirty-three!

OnePath was joined in veggie maths by BT Funds Management, Colonial First State, Auscol (Mine Super), Perpetual Super, MLC Super – whose report cards revealed “significantly poor performance”.

Some of the funds that were singled out for charging high admin fees include Verve Super (who market to women), Spaceship Super (who target millennials), Student Super (who need a detention), and the ironically named Cruelty Free Super (well, except for their barbaric admin fees).

And last but not least, Equity Trustees appear to be really struggling with their pencil grip, after being singled out by the regulator for both high fees and poor returns.

Am I being too harsh?

I don’t think so.

There is currently around $10 billion of our retirement savings sitting in underperforming funds. Many of them are not taking on new customers – because, well, who the hell would actively choose to join them?! However, they’re still more than happy to continue milking their existing customers with high fees and/or poor performance.

Why?

Because, unlike their customers, the people that run the funds are making seriously good profits!

Their only way of keeping this going is to hide their report card, and hope you forget to ask.

Don’t let them.

Tread Your Own Path!

*&^%$^* the Labor Government

I’m writing on behalf of my mum, who is distressed about the upcoming changes to superannuation. She is a widower who has worked hard all her life, saving like crazy to ensure she had a secure retirement (believing it was her responsibility not to be a burden to society via the pension) and to leave a tidy nest egg for her kids.

Hi Scott,

I’m writing on behalf of my mum, who is distressed about the upcoming changes to superannuation. She is a widower who has worked hard all her life, saving like crazy to ensure she had a secure retirement (believing it was her responsibility not to be a burden to society via the pension) and to leave a tidy nest egg for her kids.

Mum has been advised by her accountant that she is a smidge over the $3 million cap; once he wraps his head around the changes he will, I’m sure, offer her excellent advice on how to proceed. But here is my question: what the *&^%$^* is the Labor Government thinking about attacking the little nest eggs of ordinary Australians? And what the **&^^% is anyone doing about it? It appears that, despite negative press attention, the changes are going full steam ahead. It’s just not fair! Thanks for listening, Scott, as no-one else seems to be hearing our small voices of protest.

Linda

Hi Linda

I’m sure your mum must feel like she’s being unfairly targeted … and her only ‘crime’ was that she worked hard, saved harder, and made savvy financial decisions! After all, she could have just peed all her money against the wall and retired on the full pension, right?

Well, that’s true.

Yet what’s also true is that your mother is not “an ordinary Australian” and she does not have a “little nest egg”. She’s got more cheese stuffed in her super than 99.5% of the population!

And besides, as you’ve said, she has access to an accountant who will dutifully work out a way to siphon that ‘smidge’ of the tax-affected part of her $3 million balance into another low-tax environment.

So she’s going to be absolutely fine.

However, what most Australians are really worried about – and what the media have jumped on – is whether this move by the Government is the ‘thin edge of the wedge’.

So, is the media right? Is the Government really aiming to come after your super?

Bloody oath they are!

Yet that’s hardly breaking news. After all, with each passing year, politicians – on both sides – have made super less attractive. Especially for higher income earners. They’ve deliberately limited the amount you can put in each year and how much you can keep in there, and now they’re upping the taxes.

My take?

They’ll keep doing it.

Reason being, Australia has a rapidly aging population. Looking after old people is expensive. As are programs like the NDIS. Someone needs to pay for it, and the heavy lifting will come from the wealthiest people in our country.

So to your question: what’s the Labor Government doing attacking the little nest eggs of ordinary Australians?

They’re not.

It’s just that the Government isn’t in the business of providing a tax haven for wealthy people.

Or helping your mum provide a tax-effective inheritance for you.

The Government’s end game is for super to (hopefully one day) take some heat off the age pension.

So let’s talk about the “little nest eggs of ordinary Australians”:

The median super balance for Aussies aged 60–64 is just $139,056 for women and $180,928 for men … and many of these people will have to use their super to pay off their home loan when they retire!

Now that’s tough!

Scott

Help, My Dentist Wants My Super!

We have been blessed with seven kids, some of whom have unfortunately not been blessed with straight teeth. Blimey, $7,500 for braces is no walk in the park, especially when you start multiplying it by three, four or more!

Hi Scott,

We have been blessed with seven kids, some of whom have unfortunately not been blessed with straight teeth. Blimey, $7,500 for braces is no walk in the park, especially when you start multiplying it by three, four or more! Apparently, in some cases you can gain early access to your super for compassionate reasons. Do straight teeth fall into this category? Otherwise, unless I sell a kidney, there is no way I can come up with the cash. I’m 40 and have about $265,000 in super. Is it worth accessing my super early?

Dennis

Hi Dennis,

Right now I’ve got my mouth open and I’m saying “aaaah”.

The rules for a compassionate release of super are as follows:

To treat a life-threatening illness or injury, or

Alleviate acute or chronic pain, or

Alleviate an acute or chronic mental illness.

That all seems fair enough, but I don’t know how little Benny’s braces would apply to any of these.

However, I spoke to the ATO (which administers the applications) and they told me that last year 9,700 individuals applied for compassionate release of super for dental treatment expenses, and 82% were approved. Out of those approved, 9% were for a dependent child’s dental treatment, which could include braces.

Uh-huh.

So what are my thoughts?

First, with seven kids you know you’re setting an expensive precedent: if one kid gets a Hollywood smile, they all do, right?

Second, each time you dip into your super, you’re killing off the power of compound interest (plus potentially paying tax on the lump sum). In the end, it’s not going to cost you $7,500, it’s going to be something likely $30,000, or even more.

Finally, this question has given me a serious toothache.

Ultimately it’s your decision, but I’d look at every other option than raiding your super. And if you do, steer clear of these groups that have sprung up to help people access their super. Some of them charge as much as $800 to “help” you apply for the compassionate release of super. Yet it’s a basic friggin’ form that anyone can fill out in the time it takes to floss!

Keep smiling.

Scott

Vanguard Super?

I came across an article stating that Vanguard is now in the Superannuation business and will be competing against the likes of Australian Super, HostPlus etc. What is your view on this?

Hi Scott

I came across an article stating that Vanguard is now in the Superannuation business and will be competing against the likes of Australian Super, HostPlus etc. What is your view on this?

Andrew

Hi Andrew

Yes, this week Vanguard officially launched their super fund offering.

They’re charging 0.58% per annum, which is one of the lowest in the market for standard default funds with balances under $50,000.

There are cheaper superannuation index funds available.

Yet here’s what’s interesting about this:

First, Vanguard has said they’ll look to lower their fees over time as they grow. I’m inclined to believe them, because that’s what they have a history of doing.

Second, this ain’t your bog-average super fund.

Research from SuperRatings found there is a “high risk at retirement” for many of the current top-returning super funds. That’s because most of our biggest super funds throw everyone – young and old – into a one-size-fits-all investment pot.

Instead, Vanguard’s offering is a life cycle fund that invests your super based on your age. In simple terms, they automatically reduce the amount of riskier assets, like shares, in your portfolio as you get older and closer to retirement. In all, they make 36 of these adjustments up to your 83rd birthday (with no switching fees), which is far and away the most comprehensive of any Australian super offering.

So what do I think?

I think this is great news for every Australian – regardless of whether you switch to Vanguard or not.

The super fund industry trousers an outrageous $30 billion a year in fees – money that could and should be going towards our retirement.

Hopefully now that one of the world’s biggest fund managers – with a relentless focus on lowering costs – has set up shop, they’ll keep everyone on their toes.

For disclosure, I invest in some Vanguard index funds.

Scott.