Australia's Youngest Property Owner

Picture this, it’s April 26. 3:30pm.

Malcolm Turnbull and Scott Morrison are deep in the ‘burbs.

The media pack is in tow, getting ready for a photo opportunity.

Today’s pitch? That negative gearing is the way everyday Aussies (voters) get rich -- and, unlike Labor, the Government won’t mess with it.

The Prime Minister peeks through the front door and surveys the battler family.

Turnbull: “He looks ethnic. She’s a blonde. They have a baby. All my ‘demos’ covered under one roof. Excellent.”

Sco-Mo: “Mal, before we go in … there’s just one thing … the apartment. It’s for the kid.”

Turnbull: “What?!”

Sco-Mo: “It’s negatively geared … for the one-year-old.”Turnbull: “Oh for christsakes. Who organised this sh…oot? It was one of Tony’s old staffers, surely?!

Sco-Mo: “It’s too late to back out now. The cameras are rolling. Just smile. It’ll be all over soon.”

A few awkward minutes later, and with the media money shot in the can, it was all over. Yet while there was a lot of fanfare, the only person who didn’t get their say was Australia’s youngest homeowner, baby Addison. So let’s fill her in with what’s going on.

A letter to Baby Addison

Dear Addison,

Your parents love you.When I was a one-year-old all I got was second-hand cigarette smoke, and a Melbourne Footy Club beanie. Your parents bought you a home!

Now, given you’re already crawling up the property ladder, it’s time we had a grownup chat about the true costs of being a property investor in 2016. See, despite interest rates being at all-time lows, your parents will actually lose money on your apartment every single year.

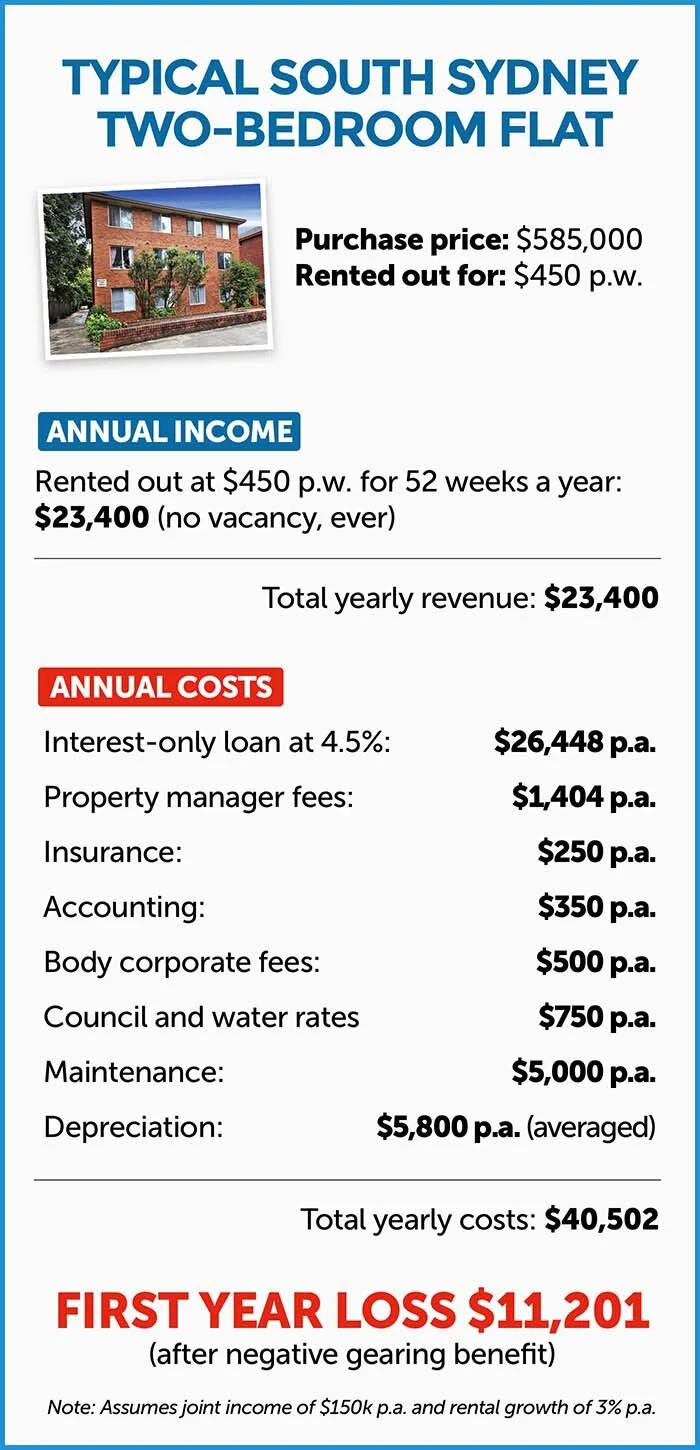

Let’s take a look at the numbers:

First, before your parents got the keys they had to shell out $22,144 in stamp duty, plus legals.

Then, even if we factor in healthy renting increases and an unlikely 100 per cent tenancy -- over the next 20 years they’ll lose $237,900 (see box).

Boo! Hiss!

Yet they’ll also get an annual negative gearing tax break, which will lessen their total after-tax losses to $155,800. Or, looked at another way, the hard-working nurse who delivered you (along with every other taxpayer) will chip in $82,100 over the next 20 years to help fund your loss-making investment.

So on very conservative figures, your parents will lose $178,944 over the next 20 years.

Now the majority of property investors today have absolutely no problem with that.But I do.I hate the idea of losing money every single year for 20 years -- even if I’m getting a tax break. Call me old-fashioned, but when I invest my hard earned money I expect my investments to put money in my pocket every single year.

And when I reinvest my returns each year, I’m getting something known as compound interest. Albert Einstein called it the eighth wonder of the world. That’s because, over time, you earn interest on your interest, and your returns snowball.

That’s the guaranteed way to get very, very rich.

But that’s not going to happen for you, unfortunately.

Your apartment won’t get the benefits of compound interest, because every last dollar of income (in the form of rent) that your parents receive, is completely gobbled up by your costs: to the bank, and to keeping the apartment. The only way your parents will make money is if the price of the apartment increases.

The Alternative: Create A Bond With Your Kid

But let’s be old-fashioned.

Instead of losing money each year, let’s save.

Now let’s run the numbers on investing the same amount that your parents will lose over the next 20 years in a low-cost, old-school investment bond, invested in an Aussie managed share fund.

For argument’s sake we’ll say your parents kick it off with $23,144 (what they paid in stamp duty and legal fees) plus what they lose (after tax) every year into the investment bond (which, as I’ve said, totals $155,800 after 20 years).

Assuming a conservative after-tax 6 per cent return, and annual investment fees of 0.78 percent, in 20 years your bond will be worth … $364,563.

A good deal for you, but an even better deal for your parents.

Here’s how I’d sell it to them, Addison.

“Mum and Dad, if you fund my future with savings, instead of debt, you’ll feel a lot less pressure. You won’t have to worry about losing your job, or not being able to fund the shortfall.”

(Which in the first year is approximately 10 per cent of your take-home pay.)

“You won’t have to worry about interest rates jacking up.”

(Let’s face it, interest rates won’t stay at a historical low for the next 20 years.)

“You won’t have to worry about your tenants breaking things, or leaving you in the lurch.”

(The figures we’ve used factor in a 100 percent tenancy over 20 years -- which won’t happen.)

“You won’t have to worry about greedy land tax grabs from the State Government.”

(They’ve got form here.)

“You won’t have to worry about changes to negative gearing.”

(Which, like changes to super, could change the game completely).

“You won’t have to worry about paying another round of stamp duty when you transfer the apartment to me in 20 years’ time.”

(Which will eat up another 4 per cent of your capital.)

“You won’t have to worry about paying capital gains tax at the end of it.”

(Investment bonds are totally free from capital gains tax free after 10 years.)

“So, Mum and Dad, for all these reasons I think you’ll agree it makes sense to save, rather than speculate. And besides, if you do, you won’t have set a precedent to buy my future brothers or sisters their own negatively geared apartment, which on these figures you won’t be able to afford … even with negative gearing!”

Tread Your Own Path!