Articles & Questions

Every week I publish a fun new article on a money topic I think you’ll find interesting. I also answer a handful of reader questions. Subscribers to my newsletter get to see everything first — but you can browse some of my past articles & questions on this page.

My Best Articles

Not sure where to start? Below I’ve handpicked a few of my favourites. And if you like what you see, don’t forget to subscribe to my free newsletter to get new issues before anyone else!

Search Articles

Chasing a Ghost

Just before Covid hit, I paid a $3,000 deposit for a new fence. Then Covid hit, and everything stopped.

Dear Scott,

Just before Covid hit, I paid a $3,000 deposit for a new fence. Then Covid hit, and everything stopped. After restrictions were lifted we got in contact with the fencer and he started all the excuses under the sun about why he wasn’t able to start the job. He finally admitted he was not going to do it. We asked for our deposit back, we still have not got it. We have told him we will take the matter to small claims court but this has made no difference to him. The trouble is we only have his first name, his bank account details, his phone number and his company name. What can I do?

Danielle

Hi Danielle,

You can do an ASIC search on his company name and find his registered details, and with that possibly take him to a small claims tribunal (like VCAT in Victoria).

So by all means, give it a go.

Having said that, he sounds like a crook. And it also sounds like this isn’t his first rodeo. So you could end up spending a lot of time, energy and emotion chasing this guy … and you still may never get the money back.

Look, I don’t want to sound too woo-woo, but sometimes you just have to let these things go …

So if it were me, I’d put that energy into finding a good tradie who’ll build you a good fence.

(And know that, one day, that guy’s going to get his nuts nailed to a fence.)

Scott.

The email came through with the subject line ‘REGRET’

Scott, My partner and I are both professionals in our early thirties. We bought a house last year and we hate it. We are struggling to adapt to a slower pace of life in the suburbs and have learnt we don’t need as much space as we thought we did.

The email came through with the subject line ‘REGRET’.

Scott,

My partner and I are both professionals in our early thirties. We bought a house last year and we hate it. We are struggling to adapt to a slower pace of life in the suburbs and have learnt we don’t need as much space as we thought we did. We feel stupid for spending a ton of money on something we can’t stand.

What are our options?”

Erica

Strewth!

There’s more emotion in Erica’s email than a midnight meltdown from my 18-month old:

They hate their new home … they feel stupid … they can’t stand it.

Well, the dream of owning your first home is a lot like parenting a newborn … the thrill rubs off disturbingly quickly … and then the reality of the responsibility sets in:

I’ve signed up for a lifetime of this?!

It’s not hard to understand why Erica is spitting the dummy.

This time last year everyone was FOMO-ing off their face. Interest rates were at all-time lows. The Reserve Bank had committed to no rate rises till 2024. Property prices had risen 30% since COVID. And that’s when Erica and her partner got property-pregnant. And that’s also when everything changed.

Today, the value of her property is going down, and the cost of her mortgage is going up. Way up. In the last three months her repayments have shot up by an extra $565 a month (based on a $600,000 loan).

And some experts are warning that house prices could drop by as much as 25%, leaving people like Erica who bought at the top in a ‘Mortgage Prison’ and unable to refinance their loan in a few years.

So what should Erica do?

Well, my advice would be to stop listening to experts about the economy. As a new property-parent you have zero fluffs to give. All it will do is freak you out and psyche you out.

I know you think you’ll never make it. But you will. You’ll grind it out, meet your mortgage repayments, and eventually get ahead. And then, in a few years, you’ll have forgotten about all the pain you went through, and you’ll trade up your family and do it all over again!

Tread your own path!

Why ING Sucks

Fiona is a young high school maths teacher who has a lot on her mind. She’s knee deep in planning her wedding, so her head is full with nuptial numbers

Fiona is a young high school maths teacher who has a lot on her mind.

She’s knee deep in planning her wedding, so her head is full with nuptial numbers:

The guest list, her wedding dress, flowers, bridesmaid dresses … bridesmaids.

One afternoon recently her phone rang.

It was a private number.

As with most people, Fiona’s reflex was to ignore it and let it go to voicemail, but then she remembered she was expecting a call from a supplier about the wedding, so she answered.

Turns out it was Telstra.

“The Telstra rep seemed to know all my details, and they ran me through the privacy stuff. Then they told me that my internet server had been compromised and that I was vulnerable to hackers”, she told me.

Fiona was a little suspicious … but the rep directed her to a Telstra website and asked her to put in her IP address. Sure enough it showed that she had in fact been hacked.

“O.M.G!”

From there, she was directed to open her emails, and then her ING banking app.

The Telstra employee (who had given Fiona her Telstra employee ID for verification purposes) asked her to write down a long series of numbers that she would need to give to the technician that would be visiting her house the next day and reset her internet.

While Fiona was busy writing down numbers, her fiancé arrived home from work and went to the study to do some banking. A few moments later he stormed out and to the lounge room and waved his ING app in her face.

The $20,000 they’d saved up in their ING account to pay for their wedding?

Gone.

Fiona had in fact been talking to a scammer all this time.

“Please make me look silly to your readers,” Fiona pleaded as she told me her story. “Because I am silly. I thought that these scams only happened to Boomers!”

Yet here’s what got my goat:

The scammers hit her account every 30 seconds, each time taking random amounts:

$546, $990, $7.50, $1,000, $99.

And they kept smashing the account until all $20,000 was drained.

Yet get this: the account name the money was going to was spelt “Drothy”.

OH COME ON!

We’re not in Kansas anymore, ING!

Grab the Tin Man and Toto and go bite these buggers!

Seriously, you’d think that Australia’s fifth largest bank – which trousered $549 million in profits after tax last year – would have tipped even just a little bit of that dough into having the most basic banking safety features … like, say, a trigger that detects when a customer is potentially getting scammed and puts a temporary lock on the account?

Nope.

Yet it gets worse.

After a lot of back and forth and tears from Fiona, ING agreed to pay her half the money back.

Half?

That makes absolutely no sense to me.

Either ING believes it’s not their problem, in which case they would tell her (politely) to go jump. Or they admit they should have detected the fraud and pay the money back.

So which is it?

You can’t get half up the duff, Drothy!

In fact, ING’s behaviour is depressingly very bank-like:

“When customers get scammed, it’s a lottery if they get reimbursed by their bank. Sometimes it’s 50%, sometimes it’s 75%, sometimes we find they get nothing”, says Gerard Brody from the Consumer Action Law Centre.

ING’s logo is a lion, which is kind of apt.

In The Wizard of Oz the cowardly lion is given a dish of courage to drink, which instantly transforms him and allows him to protect Dorothy.

Time to lick the bowl, ING.

You’re Australia’s most recommended bank. Start acting like it.

And if, dear reader, you’re thinking “There’s no way I would have fallen for a Telstra scam”, then you really need to read the following question and see how you would have fared …

Tread Your Own Path!

Rich Kid, Poor Kid … Worried Mum

We have twin girls and we recently went all in on the Barefoot pocket money strategy.

Hi Scott

We have twin girls and we recently went all in on the Barefoot pocket money strategy. One of the twins is highly motivated when it comes to jobs and earning her pocket money, while the other doesn’t care for it at all. Like AT ALL! Her ‘currency’ is connections, not money. She barely gets any pocket money each week and we’re not making up the difference, but she still doesn't care. What do you do when financial or future motivation is not an incentive for a kid?

Worried mum

Hello!

So you have a kid who isn’t materialistic in the slightest and values people over money?

Sounds like an awesome kid to me!

Here’s what I’ve learned: lecturing and hassling your kids doesn’t work.

That’s why my brand new book (due out in November) is written directly for kids.

I gave a review copy to a kid who sounds exactly like your daughter. He’s not motivated by money at all … yet he read it cover to cover and started plotting out his own small business, not to buy stuff, but to donate to Foodbank.’

Scott.

A Scammer Stole Our Family Home!

My husband and I have seven kids, aged from one to 13. Five weeks ago we finally took the plunge and bought a big family home!

Hi Scott,

My husband and I have seven kids, aged from one to 13. Five weeks ago we finally took the plunge and bought a big family home!

After the deal was done, our solicitor, Jenny, called and directed us to pay our deposit of $165,000 to the trust account. Then at 6:47am the next morning Jenny emailed us with a ‘correction’ to that account. I thought that was a bit weird, so I emailed back to confirm. Jenny came back almost immediately. All good.

So my husband took the morning off work and went to the bank to wire the money to the account. He paid the $35 bank transfer fee and made sure the teller checked and rechecked the numbers. That night we celebrated!

Then, two days ago, Jenny called to ask us where the deposit money was! Unbeknownst to her, hackers had taken over her computer and communicated with us from her exact email address, posing as her, using her exact language!

So we immediately called the police. They did an investigation and found that the scammer is in Kenya, so it was out of their jurisdiction. They also told us that Interpol doesn’t deal with ‘small amounts’. “There’s nothing you can do”, the police told us.

We have spent hours on the phone to our bank. They have given us $5,000 on the proviso that we drop any action against them. To say we are gutted is an understatement. Please alert all your readers to the risk of hackers accessing online transactions.

Nathan and Natalie

Hi Guys,

My heart absolutely breaks for you.

Here’s what you learned the hard way … that most people don’t know:

When you transfer money your bank always asks for the name of the account that you’re transferring the money to. Logically, you’d think that’s so their systems match and verify the account name.

But they don’t.

You could write ‘IMA BANK ROBBER’ in the account name and it’d still go through.

(Or ‘Drothy’, take your pick.)

Yet hang on, don’t the banks invest billions of dollars a year into cutting-edge artificial intelligence so they can cross-sell you credit cards every time you log on? Surely matching the account name would be a pretty basic code for them to add on?

Well, it turns out it is, and it works!

Five years ago banks in the Netherlands introduced account name checking and it reduced this type of fraud by a staggering 81 per cent.

So … why aren’t our banks doing it?

Well it seems it’s just not a priority for them.

But it is for me.

Nathan and Natalie, let’s make a ruckus this week, and see what happens.

Stay tuned.

Scott.

Dude, I’m HEXED!

Looks like I’m one of three million (presumably young) Australians pooping their pants about the recent announcement of a HECS index increase to 3.9%.

Hello Scott,

Looks like I’m one of three million (presumably young) Australians pooping their pants about the recent announcement of a HECS index increase to 3.9%. I’ve got a whopping HECS debt of just over $53,000 (for my two degrees which currently see me sitting in a casual position earning $26.50 per hour). In the past you’ve advised to focus on other debts or investments, rather than HECS. Does this still stand?

Lina

Hi Lina

You’re right, inflation has increased the cost of everything, including the indexation amount on HECS.

In 2021 it was just 0.6%, this year it’s 3.9%, next year … who knows?

That being said, it’s still the best debt you’ll have: your repayments are contingent on your income and, while it is tracking inflation, it’s not attracting a commercial rate of interest.

Now I don’t have a full picture of your financial situation, but it makes sense to prioritise other (higher rate) debts over your HECS.

Finally, you need to look at your return on investment:

You spent $53,000 on your education and your (admittedly short-term) return is a casual position earning $26.50 an hour?

Now that is something worth pooping your pants over.

Scott.

So about last week ...

Wow-wee! Last week’s column – on how much you need to retire – triggered an avalanche of reader responses. “That’s WAY TOO LOW!”

Wow-wee!

Last week’s column – on how much you need to retire – triggered an avalanche of reader responses.

“That’s WAY TOO LOW!”

“Are they eating baked beans in retirement?”

“You need AT LEAST $1 million to do anything half decent in retirement!”

Let’s recap:

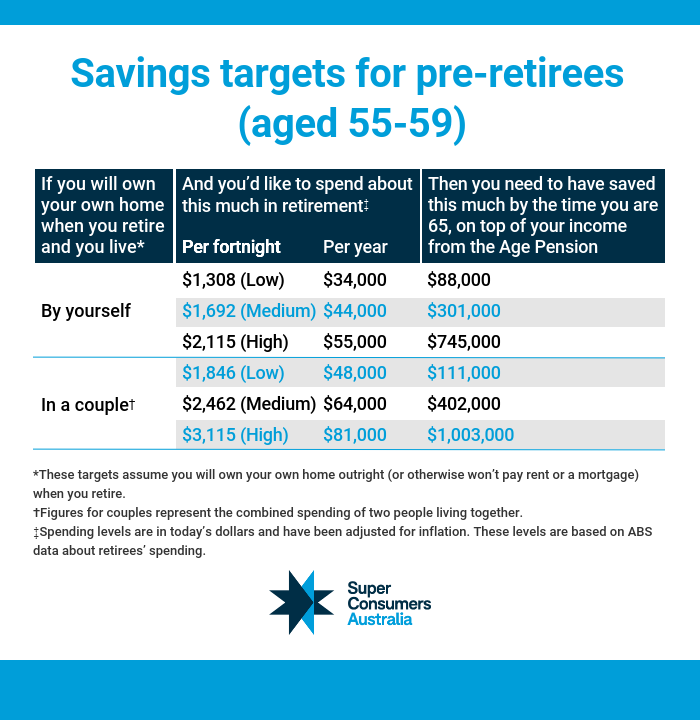

Super Consumers analysed the actual spending data of retirees, and concluded that the average home owning Aussie couple in their late 50s needs $402,000 to fund a comfortable retirement. And to be clear, that figure takes into account the rising cost of inflation, medical expenses and aged care costs.

That figure shocked a lot of readers.

‘Why was it so much less than the ‘magical million’ that always gets bandied about?’ they asked.

Well, it’s because that ‘million dollar’ retirement figure has been largely influenced by the super funds lobby ASFA (Association of Superannuation Funds of Australia), who calculate their figure for a comfortable retirement at $640,000 for a couple and $545,000 for a single.

Yet that’s not a realistic figure for the average Aussie.

In fact, according to Super Consumers, that ASFA figure is only achievable for the top 20% of retirees. And that also explains why the government’s independent Productivity Commission advised policymakers to simply ignore it!

However, the media has not ignored it – it has instead entrenched it. And in doing so it’s created a much bigger problem that affects millions of retirees, both wealthy and poor: they spend the little time they have left worrying about money, and hoarding it, instead of enjoying it.

My view?

The million dollar retirement number is a myth. It’s basically like telling a thirty-five year old, “look I’ve crunched the numbers, and if by now you’re not earning $200,000 a year, well I’m sorry but you’re going to live a crap life”.

Bugger off!

As long as you own your own home, you can live a meaningful, purposeful, retirement with much less money. After all, we have the amazingly good fortune to be living in the greatest country on earth, with a strong social safety net based on the aged pension plus subsidised medical and aged care.

And the truth is that whether you’re 35 or 65, once you’ve comfortably covered the basics, having more money won’t necessarily make you any happier.

Case in point, I spoke to a retiree this week who admitted he’d spent the best years of his life working in a job he hated so that he had ‘enough’ money to retire. Now, five years into retirement, he told me the things that really made him happy are: catching up with his daughter, watching the footy with his son, walking along the beach at low tide, and sitting on the porch in the afternoon sun. And none of them cost him a cent.

Tread Your Own Path!

Help me, help them

I’m a teacher, and I have an opportunity to put together a short finance course (10 lessons) for a Year 10 cohort at my school. I want to focus on how to set them up with really achievable, totally practical and easily applied approaches for future financial security.

Hi Scott,

I’m a teacher, and I have an opportunity to put together a short finance course (10 lessons) for a Year 10 cohort at my school. I want to focus on how to set them up with really achievable, totally practical and easily applied approaches for future financial security. There’s so much I want them to understand and so little time. What do you feel are the most critical lessons our teenagers need right now for the years ahead?

Sandra

Hi Sandra,

Kids don’t learn by lectures, but by rolling up their sleeves and doing stuff.

That’s why a few years ago I came up with my Barefoot Ten, which are ten things every kid should do before moving out. And since you need ten lessons, they could be useful inspiration. Here they are:

1. Open a zero-fee, high-interest saving account.

2. Buy and sell something second-hand.

3. Learn to cook at least two low-cost delicious, nutritious meals from scratch.

4. Volunteer in their local community.

5. Save their parents at least $100 on your household bills.

6. Promise to never, ever get a credit card.

7. Get a part-time job from age 15.

8. Earn at least one glowing reference from a boss.

9. Open up an ultra-low cost, high-growth super fund.

10. Set up a savings account for a home deposit (and nickname it even with a buck),

Feel free to steal these or create some of your own.

And if there are any primary school teachers reading … I have a book coming out in November that starts kids really early. I’ve just put the finishing touches on it. After I handed it to my editor, he said:

“This is the best book you’ve ever written.”

Scott.

Should I kick my friend out?

I’m in a difficult situation with my friend. She’s been renting my large family home from me for the last three years, paying $825 a week in rent.

Dear Scott,

I’m in a difficult situation with my friend. She’s been renting my large family home from me for the last three years, paying $825 a week in rent. I recently had a rental appraisal done and the estimated rent for the house is now between $1600-1800 per week! I’ve sent her the agent’s quote and asked her to make a decision within the month. My friend said the agent has overpriced my house and she wouldn’t pay much more than $820 per week. I know there is a housing crisis on at the moment and she has a family to consider. Help! What would be a fair thing to do? She’s already ‘unfriended’ me on Facebook!

Jocelyn

Hi Jocelyn

Thank-you for providing me with reason #784 that I am not on social media.

Look, it’s your money and not my place to judge what you do with it … but we’re not exactly quibbling over ten bucks here: you’re subsidising her to the tune of $50,000 per year!

So, you’ll have to decide whether you want to continue doing that.

If you don’t, I’d recommend hiring an agent to deal with this for you. Yes, it’s an added cost … but then again, so is the emotional cost of being unfriended on Facebook!

My advice?

Be classy, with your head held high. Tell the agent you want to give your current tenant the first right of refusal at the market rate. And if I were in your thongs, I’d be generous about giving her time to find alternate accommodation if she doesn’t want to pay the market rate.

Scott.

You Have ZERO Credibility, Barefoot

Both my sons (age 13 and 15) have read your books and are practising the ‘Buckets’ strategy. They are slowly, slowly building their wealth to financial independence using earnings from weekend chores, part-time jobs and compound interest.

Scott,

Both my sons (age 13 and 15) have read your books and are practising the ‘Buckets’ strategy. They are slowly, slowly building their wealth to financial independence using earnings from weekend chores, part-time jobs and compound interest. However, I now question your credibility and moral compass. Your misguided publication of your cringe-worthy response to the unbelievable letter claiming “my hard-working 13-year-old has saved $200,000” has left me flabbergasted. Was this a joke? What 13-year-old saves $200,000? Hardworking? Probably. Lucky and the beneficiary of an inheritance or family trust fund? Definitely. This is a slap in the face to every Aussie battler. Sadly, Scott, you have lost a reader here.

Anthony

Hi Anthony,

Congratulations, you have won my reader ‘spray of the year’ award!

So the kid in question did make the $200,000 on their own … they’re actually in the entertainment business. (However, at the parents’ request I’m not being any more specific than that.)

Yet the real issue here isn’t with the kid, it’s with you.

It sounds like you have a lot of hang-ups about wealth. Now, Anthony, your concrete is set, and you’re unlikely to change. But you don’t want your sons to inherit your anger-envy. After all, it’s totally unproductive.

Fact is, they’re going to meet wealthy people who’ve gotten money from their family. That’s life. Not everyone is equal. Not even you. (Just try comparing your salary to an average Indonesian’s.) But your sons can control one thing: the amount of effort they put in.

Scott.

Lost in Space

I am a new investor swept up in a crazy world of shares and crypto (and insane house prices). I put $5,000 in the share market using the Spaceship app, and then the market crashed!

Hey Scott,

I am a new investor swept up in a crazy world of shares and crypto (and insane house prices). I put $5,000 in the share market using the Spaceship app, and then the market crashed! Now whenever I look at my portfolio I feel queasy and want to pull it all out. Is Spaceship worth the hype, or have I thrown away my savings? And is my gut feeling to pull it out and invest in an ETF right, or should I hold on through this ‘bear market’?

Alison

Hi Alison,

Let’s you and I jump in the DeLorean and go back in time.

This time last year you were probably suffering major FOMO hearing your friends boasting about how much fast money they were making betting on Dogecoin, hot stocks and NFT-ape jpegs.

So you looked at all the investing apps and chose the one that had delivered the highest short-term returns, Spaceship. The reason it shot the lights out was because it was investing in red-hot growth stocks that investors seemingly couldn’t get enough of.

And then … investors changed their minds, sending growth stocks deep into the red. This year Apple is down 18%, as is Amazon (-35%), Tesla (-40%), Facebook’s Meta (-53%), and Netflix (-70%).

This explains why Spaceship’s flagship portfolio is down 35%.

Yet what you want to know is: where does it go next?

Honestly, I have no idea. I totally suck at market forecasts (as does every other human). And that’s why I don’t forecast. Instead, I invest in index funds that own shares in business across a range of industries. They really are set-and-forget investments, and when you combine them with low fees on many of these apps they’re great.

Scott.

Help, My Daughter Is Blackmailing Me

My adult daughter, her partner and one-year-old son are renting in a regional area and cannot afford a home loan deposit. I have offered to have them live with me rent free for six months while they save.

Dear Scott,

My adult daughter, her partner and one-year-old son are renting in a regional area and cannot afford a home loan deposit. I have offered to have them live with me rent free for six months while they save. But they want me to take it a step further and go guarantor for them. I did consider it, but as a single parent with three teens at home and a mortgage already I’m not comfortable with the risk. The problem is they are insistent that it is their only way of owning a home and that I am the only person who can help them. They have told me it will be my fault if they are homeless. I feel like they are blackmailing me. What would you do, Barefoot?

Valerie

Hi Valerie,

I’m with you.

Know this: parents all over the country are having this conversation with their kids.

It’s frustrating, because you might really want to do it. However, as they say on the plane, you need to fit your own oxygen mask before helping others. Besides, six months free rent is a bloody generous offer already!

If you feel your daughter is emotionally blackmailing you now, can you imagine what she’d do if prices continue to fall and she finds herself in a financial pickle?

Remember, as a single woman with three kids, statistically you are at the highest risk of being homeless.

Scott.

How much do you REALLY need to retire?

Let me tell you about the worst speech I’ve ever given in my life. It happened five years ago when a friend asked if I’d speak about retirement at a lunch for his men’s group.

Let me tell you about the worst speech I’ve ever given in my life.

It happened five years ago when a friend asked if I’d speak about retirement at a lunch for his men’s group.

“They’re lots of fun”, he said with a smile.

As I drove up to the gates, I realised this was no ordinary bunch of blokes: it was an exclusive private club in a wealthy suburb of Melbourne.

Specifically, two hundred slightly sozzled old guys.

I started on safe ground, talking about the state of the sharemarket.

Then I let one slip through to the keeper, explaining my Donald Bradman Strategy:

“If you own your own home, get the aged pension, and you’re willing to do a bit of paid work, you could comfortably retire on as little as $250,000”, I said matter-of-factly.

Talk about leg before wicket …

“BULLDUST!” yelled one angry multi-millionaire.

“That’s less than I paid for my yacht!” blasted another.

The crowd erupted, and basically bounced me off stage.

Howzat?!

Clearly I’d hit a nerve. After all, the number one question every pre-retiree wants to know is this:

“How much do I need in super to retire on?”

And until now there’s only been one number that everybody quotes: the Association of Superannuation Funds of Australia (ASFA) standard: $545,000 for a single and $640,000 for a couple to have a comfortable retirement.

There are two problems with this.

First, it’s out of reach for most people: the ABS says that the median super balance on retirement is $250,000 for men and $200,000 for women. So for an average working Aussie, why bother trying?

Second, the people who calculate the ASFA figure are … the super fund lobby. It’s a bit like asking old Dr Kellogg, “What’s the most important meal of the day?” (Breakfast, of course!)

Yet for years theirs was the only retirement figure available.

Until now.

A group called Super Consumers Australia (a partner of CHOICE) has done the research and come up with their own figures — and given me a sneak peek.

Not only are their figures much more attainable, they’re based on ABS research on what Aussie retirees actually spend.

So what’s their number for a comfortable retirement in these inflation-stressed times?

The newest figures are $302,000 for a single and $402,000 for a couple in a middle-income household, again assuming they don’t pay rent or a mortgage.

(This is, admittedly, a little higher than my Don Bradman figure, but that’s mainly because I encourage retirees to keep working at least a day a fortnight to supplement their income.)

Either way, for far too long the super industry has played to the millionaires in the members’ stand. What these figures do is give the average Aussie a fighting chance at scoring 100 (not out!).

Tread Your Own Path!

https://www.superconsumers.com.au/retirement-targets

Scammers Got the Lot

My daughter recently clicked on a text message from scammers saying they were from ANZ. She entered her login details and gave the scammers full access to her account.

Hi Scott,

My daughter recently clicked on a text message from scammers saying they were from ANZ. She entered her login details and gave the scammers full access to her account. I’m worried about what will happen next. I’ve googled it a bit and have seen that scammers can change your postal address and steal your identity. Is there anything my husband and I can do to help her work through this and protect her from what they might do with her info?

Kellie

Hi Kellie,

Grab your phone. Grab your daughter. Dial 1800 595 160.

That’s the number for IDCARE, Australia’s national identity and cyber support service. Their hotline is manned by specialist identity and cybersecurity counsellors who will give your daughter free advice.

Tell your daughter not to beat herself up too much. These things happen a lot. In fact, 2.1 million Aussies experienced one or more types of personal fraud in 2021, according to the Australian Bureau of Statistics (ABS). Yet, shockingly, only half of those who experienced a scam said they reported it to an authority.

Don’t let them get away with it!

Scott.

I’M FREAKING OUT!

I’m sitting here watching my portfolio plummet. The stock market is down 4.75%, and my portfolio is down 5%. IN ONE DAY. I have only been investing for a couple of years and I am freaking out. What should I do?

Hi Scott,

I’m sitting here watching my portfolio plummet. The stock market is down 4.75%, and my portfolio is down 5%. IN ONE DAY. I have only been investing for a couple of years and I am freaking out. What should I do?

Louise

Hi Louise

I feel your pain.

Now, as Warren Buffett would say … actually bugger that! All the Mr B quotes in the world can’t prepare you for your first drop in the market.

Here’s how I deal with it.

First, I don’t invest any money in the share market that I think I’ll need in the next five years.

Yes, the interest rate I’m getting sucks, but not as much as seeing the money I need evaporate in a sell off, right when I need to spend it. If you put short-term money in stocks or (god help you) crypto, you really need some time in the contemplation corner.

Second, I have come to think of my share portfolio like my farm. It’s there to provide me with a golden harvest of dividends over my lifetime. Some years there will be bumper crops, other times there will be droughts. That’s just how the world works. Yet over the long term, owning the farm makes sense (especially when I don’t have to drive a tractor to get the income!).

Finally, how do I react to savage sell offs like we had last Monday?

Well, I don’t. I feel the same way about shares falling as I do reading a newspaper headline that says ‘farm prices are down 5%’. Sure, it’s a bummer, but what can I do about it?

Call up a real estate agent and sell?

They’d be very happy to claim the commission, but would I be any better off?

Of course not!

I’m now invested in broad based, low cost index funds, and my golden rule is this: ‘never sell the farm’.

And so if I never plan on selling, what do I care about the price?

Scott.

I Have Tears in My Eyes

Six years ago we were in deep trouble. I hadn’t worked for years as I’d been looking after our young daughter, who had cancer. We’d been living on one income and had car loans, credit cards, store credit, unpaid phone bills, erratic repayment history, and a mortgage.

Hi Scott,

Six years ago we were in deep trouble. I hadn’t worked for years as I’d been looking after our young daughter, who had cancer. We’d been living on one income and had car loans, credit cards, store credit, unpaid phone bills, erratic repayment history, and a mortgage. Having enough money to cover everything seemed like a mysterious process that was only for rich people.

Well, the most incredible thing happened to us yesterday. Six years after buying your book, we have paid off our home loan and have no debt at all. It’s the most secure, calm feeling, and I am so damn proud of us.

We now have Mojo, holiday savings, shares and enough money to cover our daily expenses while still having dinners out. We’ve taught our children some massive lessons about money, and now the eldest will have her house paid off in five years.

Scott, it’s been life-changing and I write this with tears in my eyes. I’m so grateful for your book. We are ordinary people and you spoke to us in a way we could understand. The daughter who had cancer is now healthy and will soon be going for her L’s – she is busting to reach an age where she can work too! ‘Thank you’ isn’t enough but I wanted you to know it’s the best freedom I’ve ever felt and I wouldn’t have known how to get here if you hadn’t shown us the way.

Linda

Hi Linda,

Wow. Just wow. You did great!

It’s kind of amazing to me that almost seven years after I wrote my book there are still people like you coming back and telling me about their journey.

For anyone else out there who’s still working through the Barefoot Steps, I hope Linda’s story gives you some motivation. Your story is next.

Scott.

Why I Quit Drinking

It’s been almost a year since I decided to stop drinking. It all started when we headed off in the RV on our ‘lap around the map’ adventure.

It’s been almost a year since I decided to stop drinking.

It all started when we headed off in the RV on our ‘lap around the map’ adventure.

I decided – on a whim – that I didn’t really want to drink around the kids (and, besides, hangovers with four kids in a seven-metre-long van would have driven me off the road).

So I nervously announced my major life decision to Liz.

She just frowned and said:

“But you don’t even drink that much anyway!”

(She’s my rock.)

Truth be told, I always thought I’d resume drinking when I got home from our RV trip. After all, I live in the country, and when we have a boys’ night out we organise a bus to drive us both to and from the boozer. (Think about that: there’s not even the slightest thought that we’d have a light beer and drive ourselves home. Oh no, it’s on like Donkey Kong.)

So my mates think I’m weird, but I think I’m ahead of the trend.

‘Non-alcoholic drinks’ is the fastest growing drinks category in Australia. Sales of alcohol-free sauce at Dan Murphy’s have increased by more than 100% in the past two years. Perhaps that’s why when Dan Murphy’s opened their first ever bar they decided to not serve any grog. That’s right, their bar in Melbourne is called ZERO%; it serves 30 zero-alcohol drinks on tap and offers more than 200 others to take home.

Yes, being off the booze is just so hot right now. The movement even has a name – ‘Sober Curious’ – which makes me want to get rolling drunk. For me it’s right up there with Gwyneth Paltrow’s $75 vagina candle (which actually sold out, so maybe it really is a thing).

There are two factors driving this long-term trend:

First, young people are drinking more responsibly than any generation before them. According to the Centre for Alcohol Policy Research, the number of 18- to 24-year-olds who don’t drink has doubled in the past 20 years.

Second, and most importantly, non-alcoholic drinks are getting a lot better.

So my favourite beer … isn’t actually a beer. It’s called ‘Hop Valley H20’ by the Heads of Noosa Brewing Co. It’s a mix of soda water and hops, and it’s the absolute bomb. It has zero sugar, zero calories and zero alcohol. Even my old man, a seasoned drinker, likes it.

And what about wine?

Well, last month I went to see Crowded House.

When I headed to the bar, I looked up and realised that the first five drinks were all non-alcoholic. So I ordered a glass of non-alcoholic red wine and took a sip … and it blew my Barefoot socks off.

“That is the BEST non-alcoholic red wine I’ve ever tasted!” I yelled at the barman.

“That’s because it’s red wine … sorry, I must have misheard you”, he said sheepishly.

Back to the Ribena for me!

Tread Your Own Path!

From Homeless to Hero

I’m a single woman in my fifties. Not long ago I was homeless and in debt. Then I came across your book, read that apparently “I’ve Got This”, and was determined to get myself out of the hole I had dug for myself.

Hi Scott,

I’m a single woman in my fifties. Not long ago I was homeless and in debt. Then I came across your book, read that apparently “I’ve Got This”, and was determined to get myself out of the hole I had dug for myself. And I did. A couple of years on I have paid off my credit card debt, triumphantly (quietly) phoned my bank to close that account, signed a lease for a very beautiful home, bought $10,000 in ETFs, and saved $15,000 in Mojo (which gives me a huge sense of peace and freedom while I am between jobs and have no income). A big, warm thank-you for giving me and so many others such strength and hope, without shame and guilt for being in a financial mess.

Now I am wondering what people like me, who don’t have enough life left to accomplish ‘Step 4: Buy Your Home’, should do. Or have I got this too?

Sarah

Hi Sarah,

Before I get into your question, let me address the elephant in the room.

Some people would be reading your story and be shocked that you could be homeless.

However, you and I know that it’s actually pretty normal. In fact, around 400,000 women over the age of 45 are at risk of homelessness, according to a report from Social Ventures Australia.

Why?

Because older women who don’t own a home and have very little savings often end up falling through the cracks, and don’t even have access to social housing.

So should you consider taking up the Government’s Help to Buy scheme and buy with just a 2% deposit?

Heck, no!

By all means keep saving like a woman possessed. And who knows — when the time is right, you may be able to afford to comfortably buy your own home. Understand that you have already achieved financial security against all the odds … so never trade it away.

Finally, it’s human nature to forget how far you’ve come.

You went from being homeless to being debt free, owning shares and having an emergency fund behind you. Stop for a moment and celebrate it. You, Sarah, are incredible!

Keep going, you got this!

Scott.

Am I Funding the Invasion of Ukraine?

Wally, my long-suffering editor, knows he has a hot question when it’s written in ALL CAPS. Here’s one that landed last week: “AM I FUNDING THE INVASION OF UKRAINE?”

Wally, my long-suffering editor, knows he has a hot question when it’s written in ALL CAPS.

Here’s one that landed last week:

“AM I FUNDING THE INVASION OF UKRAINE?”

Wally leaned in … and it went on … and on, and on, and then took some weird tangents about Bill Gates. (Why is it always about Bill Gates?)

Anyway, the gist of the person’s question was this: he didn’t want his super to be funding war criminals (or Windows 97).

And fair enough too!

Yet, while I’ve got the tin-foil hat on, let me tell you that for well over a decade the super industry fought tooth and nail against laws that required them to disclose to investors where they were investing their money.

“Seriously, just trust us, we’re good guys!” Uh-huh.

Thankfully, the disclosure laws have now been passed, so you can see where your money is invested.

Here’s the deal. There are two ways to invest ethically within super: by choosing a dedicated ethical fund, or by selecting an ethical investment option within your existing fund.

Just understand a couple of things: first, the term ‘ethical’ is about as loose as an over-28s nightclub, so you need to dig in and see what they’re actually investing in, and whether it fits with your worldview.

Second, the fees for ethical funds and options are often much, much higher than for general investment options … which will eventually detract from your returns.

Regardless, there’s a very good chance your super fund has dumped any Russian assets it was holding. Since the start of the crisis, most funds have written off hundreds of millions of dollars of Russian investments. Yet the only way to be really sure is to call your fund and ask them.

Tread Your Own Path!

Bill Now, Pay Later?

As I was scrolling through my Facebook newsfeed drinking my morning coffee, I spotted an ad for Deferit. There are lots of ‘buy now, pay later’ schemes these days, but this is the first I’ve spotted for paying bills and splitting them into instalments.

Hi Barefoot,

As I was scrolling through my Facebook newsfeed drinking my morning coffee, I spotted an ad for Deferit. There are lots of ‘buy now, pay later’ schemes these days, but this is the first I’ve spotted for paying bills and splitting them into instalments. Although I don’t use these types of services myself, I know a growing number of people who do — so curiosity got the better of me and I had a look at what they claim to do. They claim to have no interest or late fee charges. They pay your bill up front and get you to pay it back in four equal fortnightly instalments. It appears they only charge a monthly fee when you utilise their service. My question is: is it really that transparent or is there a catch?

Sarika

Hi Sarika,

They’re basically Afterpay with a different logo.

Yet, instead of splitting $150 to get some bro-tox (why should the ladies have all the fun?), they’re suggesting you do it with your day-to-day bills.

Ding! Ding! Ding!

All these fintech bros have convinced themselves they’re saving the world. Heck, Afterpay still claims they’re a ‘budgeting app’, and so does Deferit.

Bulldust!

They’re out for themselves. The reason they encourage people to use money to pay for things is because their business model relies on it.

True budgeting advice – say, from a free financial counsellor – would get to the guts of the matter by sitting down with you, working through your budget, and looking at your capacity to pay your bills.

And this may reveal that you’re in over your head and need more than a fortnightly bandaid. Or it may help you negotiate a short payment plan with your billers so you can pay your bills with cash on time. And that will allow you to stand strongly on your own two feet.

Scott.