Articles & Questions

Every week I publish a fun new article on a money topic I think you’ll find interesting. I also answer a handful of reader questions. Subscribers to my newsletter get to see everything first — but you can browse some of my past articles & questions on this page.

My Best Articles

Not sure where to start? Below I’ve handpicked a few of my favourites. And if you like what you see, don’t forget to subscribe to my free newsletter to get new issues before anyone else!

Search Articles

Getting into Bed with Random Weirdos

Hi Barefoot, I earn $180k and have paid off my $600k home. I recently had a cold call from an investment group saying they can use the ‘income tax withholding variation’ to effectively negative-gear a property they were trying to sell us.

Hi Barefoot,

I earn $180k and have paid off my $600k home. I recently had a cold call from an investment group saying they can use the ‘income tax withholding variation’ to effectively negative-gear a property they were trying to sell us. The property is not going to be built for two years. Does this sound like a wise investment strategy?

Gerald

Hi Gerald,

The ‘income tax withholding variation’ can be downloaded from the Tax Office website. It’s not technical. Basically, all it means is that you can ask your employer to withhold less tax each payday, rather than having to wait till the end of the year for your refund.

Dude, the bottom line is that they’re really selling you a tax turkey. If you’re earning $180k you must have brains. So why are you contemplating buying a non-existent investment from random weirdos who cold call you?

Scott

Binary Tilt

Hi Scott, Can you please look into a company called Binary Tilt. They are offering very high weekly returns.

Hi Scott,

Can you please look into a company called Binary Tilt. They are offering very high weekly returns. Is it too good to be true?

Dennis

Hi Dennis,

Yes. Yes it is.

Scott

We’re in a Fix!

Hi Scott, Around 18 months ago we fixed our mortgage rate at 4.84 percent for three years, thinking it was at the bottom of the cycle.

Hi Scott,

Around 18 months ago we fixed our mortgage rate at 4.84 percent for three years, thinking it was at the bottom of the cycle. It has since dropped several times. Our minimum repayments are $378 per week, but we pay $450 on approximately $195,000. It will cost about $2,500 to get out of the fixed rate. Would we be better off financially staying put for another 18 months, or changing?

Donna

Hi Donna,

Your situation is exactly why I advise people not to fix, unless they’re on the bones of their backside.

You’re paying about 1 per cent over the odds right now -- and Commbank is forecasting we’ll get another two interest rate cuts this year (though they didn’t forecast whether they’ll actually pass them on!). Still, your relatively small loan balance means that it’s currently costing you about $100 a month.

Contrast this to your $2,500 break fee, and I think it makes sense to ride this out. But make sure you learn your lesson -- and screw down get the cheapest variable loan you can in 18 months’ time!

Scott

My Boyfriend is Moving Too Fast

Hi Scott, I am worried my partner might be doing something silly. I am 23, he is 27, and as a couple we are on about $140k a year -- with $40k in shares, $10k in Mojo, two cars paid off, no debt, no kids.

Hi Scott,

I am worried my partner might be doing something silly. I am 23, he is 27, and as a couple we are on about $140k a year -- with $40k in shares, $10k in Mojo, two cars paid off, no debt, no kids. He is thinking of buying his mother’s house for $400k as an investment property. He plans to negative gear it and is rushing to complete the sale before the election. We only have the Mojo money for the deposit. Are we moving too quickly? Could we be worse off in the long run?

Lisa

Hi Lisa,

My advice to his mum is to get an independent valuation before she sells to her son!

Now my advice to you.

What’s interesting is that you talk in terms of ‘we’ -- “we are on $140k a year”, “we only have the Mojo money for the deposit”. Yet your partner sounds like he’s an ‘I’ type of guy.

If you’re truly a partnership, you’ll make decisions as a team.

Personally, I’d never make a major financial decision that my wife wasn’t fully on board with.

That’s not only because we’re a team, but because I respect her opinion. Women tend to have a sixth sense of ‘safety’ when it comes to money that most hunter-gathering blokes don’t have. (Maybe that’s sexist, or maybe I just have an amazing wife.)

Bottom line: if he’s not willing to consult you on your concerns -- and he expects you to put your money in -- then my advice would be to stop thinking about your money as ‘ours’ and more about it as ‘mine’.

Scott

The dirtiest, slimiest, most heartbreaking scam of them all.

This week, it’s National Consumer Fraud Week. And today I’m going to talk to you about the dirtiest, slimiest, most heartbreaking scam of them all.

This week, it’s National Consumer Fraud Week.

And today I’m going to talk to you about the dirtiest, slimiest, most heartbreaking scam of them all.

(No, it’s not the Nant Distillery in Tasmania -- although I’ve got my eye on you guys.)

What makes this scam so shocking is that it’s an ‘inside job’. And it happens every single day.

Here’s a real-world example, courtesy of a woman who rang my radio show a few years back:

Woman: “A year ago my mum had to go into a nursing home because she has dementia. She has almost $115k in savings which she no longer has any use for, and I have a son who has just been accepted into acting school in New York.

My siblings and I are wondering what the cost implications would be if we take the money out now and divide it between the family.

Will we pay more tax doing it that way?”

Barefoot: “Can’t you wait until the poor woman dies?”

Woman: “Sorry?”

Barefoot: “You are stealing her money.”

Woman: “No, I’m calling because I want to know about the tax implications of…”

Barefoot: “No, you are stealing her money.”

Woman: “She doesn’t need it.”

Barefoot: “Who says?”

Woman: “I do!”(And with that the woman hung up on me.)

The Worst Scam in the World

Clearly, this woman didn’t feel that she was doing anything wrong.In her mind, she and her siblings were going to get the money eventually … why not just speed it up?

This is known in the industry as ‘inheritance impatience’.

Though I prefer to call it ‘Granny Greed’ (or Grandpa Greed).

“It’s pretty consistent,” says Greg Mahney, the CEO of Advocare.“Research shows that about 1 in 20 will experience some form of elder abuse, and the most common is financial abuse.”

Though no one really knows the true figure of course.

After all, what parent wants to admit their family are ripping them off?

And sadly, it mostly is family that do the damage: the latest research from Advocare suggests that 89 per cent of perpetrators are family members.

We’re not talking peanuts either. In the 2013-14 financial year, the Elder Abuse Prevention Unit in Queensland uncovered 139 older people who were ripped off to the tune of $56.7 million in total. And that’s just in one state.

Statistics are one thing, but let’s look at three real-life case studies, given to me by Advocare:

Case Study 1: Down in the Dumpster

An elderly woman lived in a nursing home while her son took care of her home. He got her to sign some paperwork for bills relating to the house, which she did without checking. An aged care advocate drove past her home later that day and saw that her possessions were being thrown into a skip, and a ‘for sale’ sign was placed on her home. He’d had her sign an authority to sell.

Case Study 2: Granny Falls Flat

An elderly woman sold her house and gave the proceeds to her daughter and son-in-law, so they could build a granny flat onto their home, where she could live for the rest of her life. A few years later, the couple divorced and the family home was sold in the separation of assets. It severely limited her aged care options.

Case Study 3: The One-armed Bandit

A frail elderly man living in a retirement home gave his daughter his ATM card to get some basics from the shops. An aged care advocate checked their bank account and found thousands of dollars of unauthorised transactions -- from pokie venues.

Here’s the thing: most of the kids get away with it.

Why?

First, it’s the circle of life (as Elton John sang). Elderly parents often rely on their kids to dish out their pills, feed them, clothe them and drive them around. They rely on them.

Second, they’re coming to the end of their lives and don’t want to harbour a grudge.

Third, there’s the grandkids.

Heavy, huh?

Well, mark my words, this is going to become a much bigger problem, for a few reasons.

The property boom has many oldies living in million-dollar homes while their kids and grandkids struggle under the weight of massive mortgages. Rising superannuation has meant that we’re creating the wealthiest generation to ever retire. And then there’s another boom: it’s predicted that by 2050 in Australia people aged 65 and over will double, and dementia will triple.

So what can you do to protect your ageing loved ones?

Well, on a practical level, you need to ensure that your entire family are on the same page, and that they respect your parents’ wishes -- even if they don’t agree with them.And make sure that everything is documented with an independent legal expert -- keeping a close eye for the idiot brother-in-law who’s always scratching around with a sob story looking for a ‘loan’.

The other thing to do is appoint two enduring powers of attorney:

One from the family and one from outside the family (preferably a trusted friend or even a lawyer) who doesn’t have dibs on Aunt Mavis’s BHP shares in the will. If they’re appointed jointly, it means they’ll have to make their decisions jointly.

And hopefully they’ll act in the best interest of the person who matters most.

Tread Your Own Path!

The Banker and the Dog

Scott, My wife and I are 40, with two primary-school-aged kids. I seek your investment opinion.

Scott,

My wife and I are 40, with two primary-school-aged kids. I seek your investment opinion. We are now mortgage and debt free, with $2 million in cash due to an inheritance. Our investment goals: long-term growth combined with cashflow return to earn $40k p.a. We are thinking 70 per cent in property and 30 per cent in shares. Our banker suggested UBS Callable Goals, which is linked to four Australian bank shares, maximum 3-year, which pays an 8 percent fixed coupon. What would you do?

Danny

Hi Danny,

OK, here’s what I took out of your question:

You’ve done well! The only thing that could hurt you now is if your friendly banker works out that you’ve got 2 million large burning a hole in your pocket.

I had a glance at the ‘UBS Callable Goals’ product he recommended you. My first thought was: ‘this is a pile of dog turd’, but on second thoughts, I don’t want to disrespect my dogs do-dos. It looks like a bunch of very smart bankers have conjured up a confusing product so they can make a boatload of fees (up to 3.75 per cent up front, apparently).

Yes, they’re headlining that you can get a potential return of 8 per cent (by writing options against bank shares), but the fine print shows that if there’s a ‘kick-in event’ you could lose 65 percent of your investment. But win, lose or draw, you still pay the bankers their fees.

Dude. You have $2 million bucks, so quit playing these silly games. A 5 percent dividend yield from a few old-fashioned, low-cost listed investment companies will generate you $100,000 a year. Peace.

Scott

Wife Doesn’t Want to Be Twenty Again

Hi Scott, My wife and I are both 53. I earn $110k but our living costs are consuming our income, leaving nothing for extras or contingencies.

Hi Scott,

My wife and I are both 53. I earn $110k but our living costs are consuming our income, leaving nothing for extras or contingencies. We have exhausted our savings and rung up $24.5k in credit card debt, with another $8.5k drawn against our home -- which is worth $500k, with $403k owing. We have an investment townhouse in Brisbane worth $370k, with $322k owing. Our refinancing options are limited as our debts are equal to 85 percent of our assets. The way my wife puts it, she does not want to ‘go back to living like we did in our 20s’. What are our options?

Lindsey

Hi Lindsey,

Sounds like your wife is half the problem (and … you’re the other half). She may say she doesn’t want to live like you did in your 20s, but you guys are behaving like it. You’re 10 years out from your retirement and you’re funding your lifestyle by credit cards? Seriously?!

Yes, you can sell the townhouse, which will pay off your credit card debts, and maybe your line of credit (remember, though, you’ll pay capital gains tax). However, it’s a near certainty that you’ll end up right back where you are now unless the two if you get on the same page. And by that I mean convince your wife that there’s more long-term pleasure in being financially secure than there is mindlessly adding to the nation’s landfill.

Scott

Budget Horror

Hi Scott, I am one of your Barefoot buddies. I write as I am greatly concerned about the proposed Budget changes to superannuation.

Hi Scott,

I am one of your Barefoot buddies. I write as I am greatly concerned about the proposed Budget changes to superannuation. I am 58 and I have four investment properties on which I have significant debt. A month or so ago I decided I would sell the properties, pay off the debt and put the profit into superannuation. I was hoping to get around $1.5 million into super (I currently have $300,000).

After the Budget I am limited to a lifetime cap of $500,000. What makes me angry is that the Government has said that people can have up to $1.6 million in super when they start a pension phase, but the new rules will not allow me to reach the cap. This all seems grossly unfair to me. What can I do?

Renae

Hi Renae,

Well, you can vote Labor! Their super policy will allow you to contribute $180k a year post-tax into super.

But, other than cosying up to Bill, let’s see what you can do:

Yes, you’re dead right -- the changes to super in the Budget are aimed at limiting the amount of money that wealthy people can invest into super in the future. But on the brightside, you’ve got $1.8 million in investable assets. That’s a very first world problem you’re suffering.

On a practical level, so long as you haven’t made a post-tax contribution since 1 July 2007, you’ll be able to contribute $500,000. If you’re married, your hubby could do the same in his fund. You can also make a pre-tax contribution of $25k a year until you’re 75 without having to satisfy a work test.

To be honest, though, super laws these days are about as reliable as a Donald Trump election promise. You get the feeling that, eventually, whoever ends up in charge will build a giant wall around super and tax the hell out of it.

Scott

My Girlfriend is in Hell

Scott, My girlfriend is stuck in financial hell. Her estranged husband, who lives upstairs, is a gambler and has lost it all, a couple of times.

Scott,

My girlfriend is stuck in financial hell. Her estranged husband, who lives upstairs, is a gambler and has lost it all, a couple of times. The house they live in is in held in trust by his parents. She has started her own business (cleaning) and is doing well. She has the income … until he steals it. Who does she go to? She has no assets, just cash hidden. She wants to run, but can't. He has taken out loans in her name in the past. So how can she get a loan to buy a house?

Tom

Hi Tom,

Intense! And … a little bizarre.If things are as bad as you say they are, you should encourage her to leave and start the process of a formal separation. She should also immediately shut down any joint accounts she has with him. If there’s a silver lining it’s that she’s in a slightly better situation than some women, in that she’s earning a decent income that will hopefully tide her over (in a rental property) until her situation becomes clearer.

Scott

Australia's Youngest Property Owner

Picture this, it’s April 26. 3:30pm.

Picture this, it’s April 26. 3:30pm.

Malcolm Turnbull and Scott Morrison are deep in the ‘burbs.

The media pack is in tow, getting ready for a photo opportunity.

Today’s pitch? That negative gearing is the way everyday Aussies (voters) get rich -- and, unlike Labor, the Government won’t mess with it.

The Prime Minister peeks through the front door and surveys the battler family.

Turnbull: “He looks ethnic. She’s a blonde. They have a baby. All my ‘demos’ covered under one roof. Excellent.”

Sco-Mo: “Mal, before we go in … there’s just one thing … the apartment. It’s for the kid.”

Turnbull: “What?!”

Sco-Mo: “It’s negatively geared … for the one-year-old.”Turnbull: “Oh for christsakes. Who organised this sh…oot? It was one of Tony’s old staffers, surely?!

Sco-Mo: “It’s too late to back out now. The cameras are rolling. Just smile. It’ll be all over soon.”

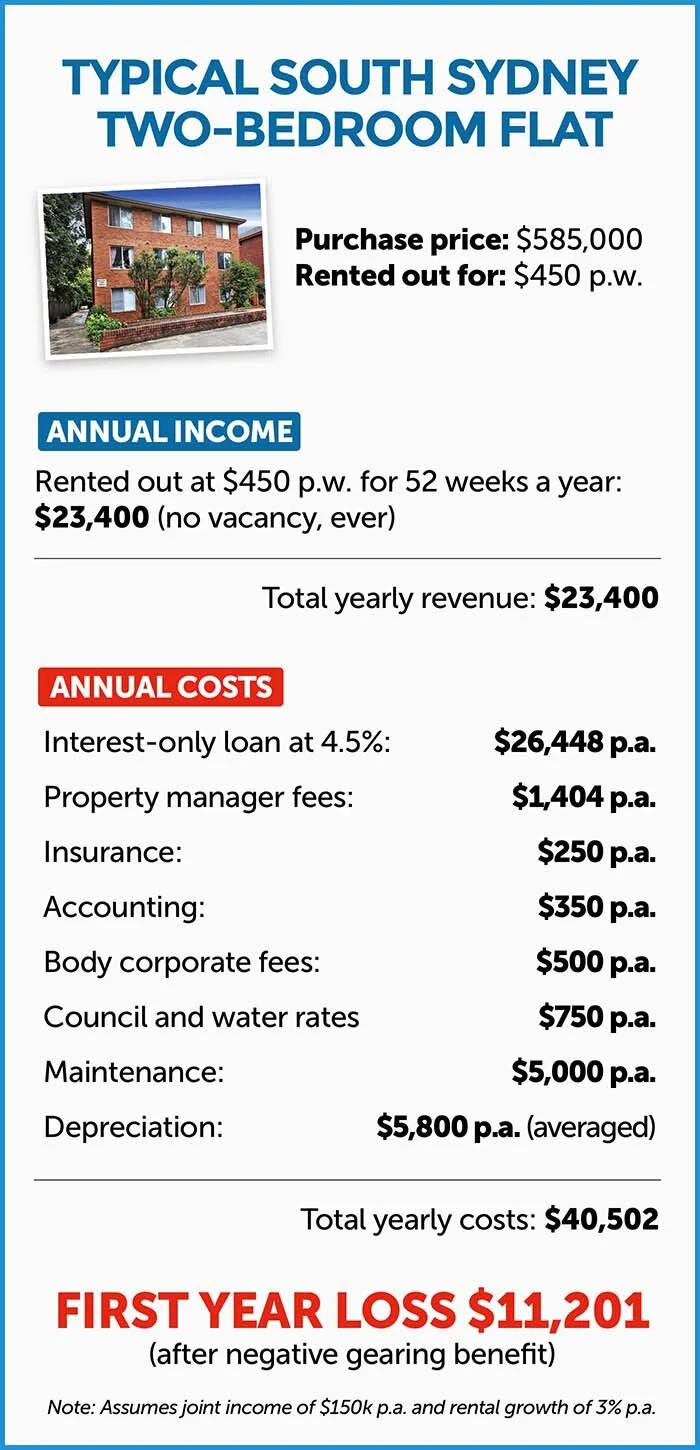

A few awkward minutes later, and with the media money shot in the can, it was all over. Yet while there was a lot of fanfare, the only person who didn’t get their say was Australia’s youngest homeowner, baby Addison. So let’s fill her in with what’s going on.

A letter to Baby Addison

Dear Addison,

Your parents love you.When I was a one-year-old all I got was second-hand cigarette smoke, and a Melbourne Footy Club beanie. Your parents bought you a home!

Now, given you’re already crawling up the property ladder, it’s time we had a grownup chat about the true costs of being a property investor in 2016. See, despite interest rates being at all-time lows, your parents will actually lose money on your apartment every single year.

Let’s take a look at the numbers:

First, before your parents got the keys they had to shell out $22,144 in stamp duty, plus legals.

Then, even if we factor in healthy renting increases and an unlikely 100 per cent tenancy -- over the next 20 years they’ll lose $237,900 (see box).

Boo! Hiss!

Yet they’ll also get an annual negative gearing tax break, which will lessen their total after-tax losses to $155,800. Or, looked at another way, the hard-working nurse who delivered you (along with every other taxpayer) will chip in $82,100 over the next 20 years to help fund your loss-making investment.

So on very conservative figures, your parents will lose $178,944 over the next 20 years.

Now the majority of property investors today have absolutely no problem with that.But I do.I hate the idea of losing money every single year for 20 years -- even if I’m getting a tax break. Call me old-fashioned, but when I invest my hard earned money I expect my investments to put money in my pocket every single year.

And when I reinvest my returns each year, I’m getting something known as compound interest. Albert Einstein called it the eighth wonder of the world. That’s because, over time, you earn interest on your interest, and your returns snowball.

That’s the guaranteed way to get very, very rich.

But that’s not going to happen for you, unfortunately.

Your apartment won’t get the benefits of compound interest, because every last dollar of income (in the form of rent) that your parents receive, is completely gobbled up by your costs: to the bank, and to keeping the apartment. The only way your parents will make money is if the price of the apartment increases.

The Alternative: Create A Bond With Your Kid

But let’s be old-fashioned.

Instead of losing money each year, let’s save.

Now let’s run the numbers on investing the same amount that your parents will lose over the next 20 years in a low-cost, old-school investment bond, invested in an Aussie managed share fund.

For argument’s sake we’ll say your parents kick it off with $23,144 (what they paid in stamp duty and legal fees) plus what they lose (after tax) every year into the investment bond (which, as I’ve said, totals $155,800 after 20 years).

Assuming a conservative after-tax 6 per cent return, and annual investment fees of 0.78 percent, in 20 years your bond will be worth … $364,563.

A good deal for you, but an even better deal for your parents.

Here’s how I’d sell it to them, Addison.

“Mum and Dad, if you fund my future with savings, instead of debt, you’ll feel a lot less pressure. You won’t have to worry about losing your job, or not being able to fund the shortfall.”

(Which in the first year is approximately 10 per cent of your take-home pay.)

“You won’t have to worry about interest rates jacking up.”

(Let’s face it, interest rates won’t stay at a historical low for the next 20 years.)

“You won’t have to worry about your tenants breaking things, or leaving you in the lurch.”

(The figures we’ve used factor in a 100 percent tenancy over 20 years -- which won’t happen.)

“You won’t have to worry about greedy land tax grabs from the State Government.”

(They’ve got form here.)

“You won’t have to worry about changes to negative gearing.”

(Which, like changes to super, could change the game completely).

“You won’t have to worry about paying another round of stamp duty when you transfer the apartment to me in 20 years’ time.”

(Which will eat up another 4 per cent of your capital.)

“You won’t have to worry about paying capital gains tax at the end of it.”

(Investment bonds are totally free from capital gains tax free after 10 years.)

“So, Mum and Dad, for all these reasons I think you’ll agree it makes sense to save, rather than speculate. And besides, if you do, you won’t have set a precedent to buy my future brothers or sisters their own negatively geared apartment, which on these figures you won’t be able to afford … even with negative gearing!”

Tread Your Own Path!

My Variable Income

Hi Barefoot. I like your stuff and follow it pretty closely.

Hi Barefoot.

I like your stuff and follow it pretty closely. As a result of that, and some hard work, we are doing okay.

We have just started our own business, but because we’re starting out we don’t draw a wage for my husband, so my job pays the bills. We’re making money on paper, though cashflow is a killer. I get the idea of your 60/20/20 rule when there’s a consistent income --- but where on earth should we start when one of us is self-employed?

Nikki

Hi Nikki,

Fantastic question!

The 60-20-20 Rule involves screwing down your living costs to 60 percent of your income and then devoting 20 percent to savings and 20 percent to splurging.

And you know what? It’s actually the perfect plan for people on a variable income.

Why?

Well, you may not know how much money you’ll earn, but you know how much you have to spend to keep the lights on and beer in the fridge. Your business needs to cover that figure, and your superannuation, as a minimum. If it’s not, make changes in the business until it does, or, if it’s never going to happen, get out of the business.

When you earn more than your basics, plough that money into your savings. As a small business owner myself, I have three months of personal living expenses and three months of business expenses sitting by. Being your own boss can be brutal -- so stack the odds in your favour.

Scott

When Are You Going to Apologise?

When are you going to apologise to your readers for your stupid advice!? They really will be ‘barefoot’ if they keep their ‘Mojo’ in a savings account, now the Reserve Bank has cut interest rates to a historical low of 1.

When are you going to apologise to your readers for your stupid advice!? They really will be ‘barefoot’ if they keep their ‘Mojo’ in a savings account, now the Reserve Bank has cut interest rates to a historical low of 1.75 percent! They won’t even have money to buy shoes!

Tony

Hi Tony!

I’ll take your exclamation marks and raise you!In all the time I’ve been Barefoot, I’ve never had anyone write to me and say “You bastard, Barefoot! The worst thing I ever did was take your advice and save some money so I could get some financial breathing space!”

Seriously, Tony, I view my Mojo savings the same way that way Warren Buffett sees the billion he has perpetually parked in zero-percent-returning US treasury bonds: the return is peace of mind ... and the ability to be greedy when other people are fearful.

Scott

The Rocking Chair Test

Hi Barefoot, My wife and I are both 30 and we are lucky enough to earn a combined $350k per annum. Our living costs are $40k a year now, though kids may happen.

Hi Barefoot,

My wife and I are both 30 and we are lucky enough to earn a combined $350k per annum. Our living costs are $40k a year now, though kids may happen. Last year we paid off our mortgage, and we have a combined $200k in savings and $130k in super. We grudgingly admit that some risk is necessary, but find investing stressful and confusing, so we want minimal involvement. What is the best low-stress, set-and-forget strategy to retire on our own timeline (not when the government lets us access super)?

Max

Hi Max,

At the tender age of 30 you’re basically at the financial finish line, while most of your mates are still on the starting blocks. Respect. Also, your living expenses are very low for your income, which is a sign that you’re not wankers. More respect.

Here’s my practical advice: set up a family trust and invest a set amount into low-cost listed investment companies (LICs) or direct shares every single month. That’s how you take the confusion and stress out of it. Keep it simple, and it’s likely you’ll be multimillionaires by the time you hit your 40s.

From that point on, your life won’t materially change -- regardless of how many millions you eventually pile up. So I’d encourage you to do a little exercise: imagine you’re sitting side by side in rocking chairs 40 years from now, looking back at your lives. What did you devote yourself to? Who did you help? What change did you make? What are you proud of? Then do it.

Scott

Please Help, I’m Desperate

Hi Scott, In one of your recent newspaper columns you exposed the Tasmanian whisky operator Nant Distilling Company, warning your readers to steer clear of them. I was not so lucky.

Hi Scott,

In one of your recent newspaper columns you exposed the Tasmanian whisky operator Nant Distilling Company, warning your readers to steer clear of them. I was not so lucky. I have $15,000 invested with Nant, and I am finding it all but impossible to get them to honour their ‘buy back’ promise, even though I have abided by the agreement. I have rung the company at least 20 times. I even had an email from an operations manager agreeing to pay me out, but he has since left the company, so I am back to square one. Is there anything you can do?

Fraser

Hi Fraser,

What can I do?

Well, I’ve warned investors (and retired cricketer Matthew Hayden, who was spruiking for them) just how horrible I believe this business is. Seriously, an investment in Nant is much the same as a teenager’s first binge-drinking experiment with whisky -- In both cases you’re likely to end up shivering in a dunny, covered in vomit.

Sadly, I don’t think you’ll get any help from the regulators either. Reason being, when I was investigating Nant they were at pains to point out that they weren’t marketing an investment product -- which would see them regulated by ASIC, the corporate cops. Instead they argued that they are simply selling whisky.

Yet here’s Nant’s pitch to SMSF investors taken directly from their website: “Our unique barrel buy-back program offers you an equivalent return of 9.55% compounded annually, paid when you sell your barrel back to Nant after four years maturation.”

So what happens if Nant decides not to buy back the barrels?

Well, you’ll get … nant!The worst thing about Nant is that they’re still flogging their investments -- sorry, whisky barrels -- to unsuspecting investors, even though it appears they’re not paying out existing investors like you.

Seriously, though, I called Nant on your behalf, and they assure me that ‘everything is fine’, and that you’ll get your money back, in a few months. Perhaps. Maybe. Depending on the maturation process (and testing) of your whisky.

Scott

The Most Important Investment Lesson In The World

“If you stick around till lunch, I’ll share with you what I believe is the most important investment lesson in the world”, Warren Buffett told me (okay, and 40,000 others) in Omaha last weekend at the Berkshire Hathaway annual meeting. At which point my old man, an Omaha virgin, elbowed me in the ribs and said with a grin, “This is what we came here for”.

“If you stick around till lunch, I’ll share with you what I believe is the most important investment lesson in the world”, Warren Buffett told me (okay, and 40,000 others) in Omaha last weekend at the Berkshire Hathaway annual meeting.

At which point my old man, an Omaha virgin, elbowed me in the ribs and said with a grin, “This is what we came here for”.What was Buffett’s secret?Smart beta? Emerging markets? Hedge funds?

Nope.

But if you’re a bloke from, say, Ouyen, it’s not a bad guess.

After all, it’s not hard to be intimidated by the world of high finance. Billionaires. Private jets. Sophisticated finance-speak.

Let’s face it, no one living in suburbia gets access to the hottest hedge funds on Wall Street. They’re closed shops. You need serious bucks and high-finance connections to get access to the most exclusive funds run by the sharpest investors in the world.

The refreshing news is that Buffett has spent years poking fun at Wall Street.

And, as always, he’s put his money where his mouth is.

You see, back in 2007 (when I was an Omaha virgin myself), Buffett made a famous million-dollar bet.He bet that a basic, no-brainer index fund that simply tracks the market will outperform the most elite hedge funds over 10 years.

A New York firm, Protégé Partners, took Buffett at his word and put their money into five of the best hedge funds they could find. We’re talking incredibly smart money managers with highly sophisticated strategies. They can bet against the market, they can get in and out of the market when they want, and they can scan the world for the best opportunities.

It was certainly a ballsy bet from Buffett -- particularly since the timeframe would include the Global Financial Crisis (a time when the index tracker, well, tracked the market straight over a cliff).

Back to Omaha.

Lunchtime came around, and Buffett gave his highly anticipated speech.

He began by putting up a slide showing how his million-dollar bet was going.

You guessed it: the no-brainer index fund had wiped the floor with the high-fee hedge funds -- outperforming them, to date, by a staggering 40 per cent.

Here starteth the lesson.

(As you read this, understand that Buffett is referring to stockbrokers, highly paid fund managers, financial planners and asset consultants.)

Over to Mr B:“Supposedly sophisticated people, generally richer people, hire investment consultants. And no consultant in the world is going to tell you, ‘just buy an S&P index fund and sit for the next 50 years’. You don’t get to be a consultant that way, and you certainly don’t get an annual fee that way.

“So the consultant has every motivation in the world to tell you, ‘this year I think we should concentrate more on international stocks’, or ‘this manager is particularly good on the short side’. And so they come in and they talk for hours, and you pay them a large fee, and they always suggest something other than just sitting on your rear end. And then those consultants, after they get their fees, they in turn recommend you to other people who charge fees, which … cumulatively eat up capital like crazy.

“And they always change their recommendations a little bit from year to year. They can’t change them 100% because then it would look like they didn’t know what they were doing the year before.

“I’ve talked to huge pension funds, and I’ve taken them through the math, and when I leave, they go out and hire a bunch of consultants and pay them a lot of money”, said Buffett as the crowd roared with laughter.

At this point, Buffett’s sidekick and Berkshire Vice Chairman, Charlie Munger (who is a sprightly 92 years old and who’d consumed more Coca-Cola and peanut brittle throughout the day than was at my three-years-old’s last birthday party), chimed in and said:

“Warren, you’re talking to a bunch of people who have solved their problem by buying Berkshire Hathaway … and that has worked out even better.”

He’s right.

From 1965 through to the end of last year, Berkshire shares have risen 1,598,284 percent, versus the S&P 500’s 11,355 percent (and less for most professionally managed funds).

In a few words, Buffett’s investment lesson was this: don’t pay over-the-top fees.

And I agree wholeheartedly. (At Barefoot, we have our own independent investment newsletter which has consistently beaten the market by focusing on ultra-low-cost funds and savvy stock picks.)

Says Buffett: “There’s been far, far, far more money made by people in Wall Street through salesmanship abilities than through investment abilities.”

Tread Your Own Path!

The Gag Falls Flat

What I took out of the deliberately boring budget, is that young first home buyers are screwed.

The government is clearly making property prices an election platform. That’s why they’re not touching negative gearing -- despite the fact that the Prime Minister has referred to it as an ‘excess’ in the past.

Coupled with that, the retrospective changes to super (cutting what you can put into super, both pre and post tax, and limiting how much you can hold), means many high income earners will divert their cash from super to property.

Finally, when you add in this week’s interest rate cut to a historic low of 1.75 per cent (with more to come), you can see what I mean when I say that young people are screwed.

The Prime Minister, in full election mode, suggested on morning radio that wealthy parents should ‘shell out’ to buy their kids a home. Okay, so it was meant to be a gag, but it was in poor taste for the millions of young families who are struggling to save up for a deposit.

Truth is my parents couldn’t afford to buy me a house. And I wouldn’t have wanted them to anyway. Saving up a deposit and buying a home under your own steam is one of life's great achievements. It’s a pity that this government doesn’t understand that, and instead makes it even harder.

Reminder: I first wrote about this years ago and highlighted the low costs. Today there are better deals on offer. How do I know? Because my readers constantly email me about them! So before you do anything, do a quick google.

Don’t Believe the Hype

Hello Scott,I don't have a question. I just want to congratulate you on your commonsense approach to financial issues.

Hello Scott,

I don't have a question. I just want to congratulate you on your commonsense approach to financial issues. You stand for self-responsibility, hard work, living within your means, and using time as a path to financial security. I have managed to achieve a comfortable retirement through these principles, not from any great windfall. You avoid the hype and doomsday predictions of other so-called experts and focus on what an individual can do within their own life. Well done.

Bill

Thanks Bill!

I’ve been writing this column for 11 years, and people complain and congratulate me on the exact same thing: ‘Your stuff is just common sense!’ Maybe it’s just not that common these days?

Scott

Widow Learns a Lesson?

Hi Scott,I recently lost my beautiful husband unexpectedly. Unfortunately we didn't have a will.

Hi Scott,

I recently lost my beautiful husband unexpectedly. Unfortunately we didn't have a will. It’s been a stressful and expensive lesson, I want to make a will but don't really want to pay hefty solicitor fees. What do you think about 'do it yourself' will kits?

I don't own any property and just want to protect my savings and super and leave it to my chosen beneficiaries.

Deb

Hi Deb,

There’s a question behind this question…You’ve been through a traumatic, totally life-changing event.

You don’t need a will kit. You need a plan. I’d recommend you sit down with a financial advisor (talk to your not-for-profit super fund). Explain that you need a plan to protect and grow your savings, and a plan to manage your estate – which will include drawing up a simple low-cost will by a solicitor, and completing binding nomination forms for your super. Think of this as an investment in peace of mind.

Scott

Help! My Partner Left Me Poor

HI Scott, My partner left me in a poor financial state when he broke up with me. My house is worth $275k and I own $90k of it.

HI Scott,

My partner left me in a poor financial state when he broke up with me. My house is worth $275k and I own $90k of it. I have $110k of superannuation, I earn $95k and I am 51 years old. I want to retire at 65. So, should I sell my house and try to buy a unit at around $280k on an interest only loan and salary sacrifice the balance of what I used to pay on my home loan into my super, or should I try to pay off my unit once I've bought it?

Wendy

Hi Wendy,

Hang around my inbox for a while Wendy, and you’ll find thousands of people who would happily trade places with you: you’re young, you’ve got equity in your place, and you’ve got more super than most women. Life is good. Now let’s make it better.

First things first: there’s no reason to sell your current home – you can refinance your existing home loan to interest only – though I wouldn’t recommend it.

Instead, I’d stay where you are, and aim to have it paid off by the time you retire – at 67 (let’s tack on another two years of work).

If you pay $1550 a month off your home loan, you’ll be on track to be debt free when you retire (though understand interest rates will likely increase over the next 16 years).

If you can get your non-mortgage living expenses down to about $2,500 a month, you’ll beable to salary sacrifice $1700 a month into your low-cost growth-orientated superannuation fund. And if you can do that, you’ll be on track to retire with a balance of $560,000.

Scott

Can We Buy a Million-Dollar First Home?

Hi Barefoot, My husband and I have a goal of buying a house in four or five years. Our goal is to have a 20 per cent deposit for a $1 million dollar house.

Hi Barefoot,

My husband and I have a goal of buying a house in four or five years. Our goal is to have a 20 per cent deposit for a $1 million dollar house. Big goal, but even if we miss the mark we will still have a good deposit. My question is: Is it possible to save this amount of money while living by your 60-20-20 rule? Basic maths says no. We earn $128,000 before tax between us and presume this will go up soon. We also wish to start a family in a year or so. Are we being ridiculous?

Naomi and Ben

Hi Guys,

Yes, you are being ridiculous.However, you’re in good company. I meet a lot of newly married couples that want to do in 5 years, what took their parents 25 years.

So let’s have an adult conversation: you can’t afford to buy a million dollar home because you’re earning $128,000 a year, and because you’re about to start a family. You simply aren’t earning enough. Besides, your goal shouldn’t be to buy a million dollar home -- it should be to own your own modest family home outright in fifteen years. That’s probably how your family did it.

Scott

My Knight In Shining Armour Has Arrived!

Hi Scott, My knight in shining armour showed up! The trouble is, with him came the henchmen that are credit card debt, a Cash Converters loan, a jewellery store loan (from when he proposed to his ex), and a monster Telstra bill -- all up around $15,000.

Hi Scott,

My knight in shining armour showed up! The trouble is, with him came the henchmen that are credit card debt, a Cash Converters loan, a jewellery store loan (from when he proposed to his ex), and a monster Telstra bill -- all up around $15,000. Where do we get copies of all these bills, and how do we go about paying them off? He earns $110,000 and can have them smashed out in a matter of months, I reckon.

Amanda

Hi Amanda,

It sounds like he’s been a bit loose with his lenders, so I’d suggest he gets a copy of his credit file (if he writes to VEDA, they legally have to provide him with a free copy). It’s the financial equivalent of an STD test – if there’s a nasty surprise, it’ll be on that file.

Now from a logical standpoint, your fella should be able to smash his debt out in a matter of months: he’s earning around $6,600 a month after tax. Yet people get themselves into financial strife, (and stay there) for all sorts of illogical reasons.

So here’s my tip for you.

Make your knight in shining armour pass one final test before he gets the hand of you, his princess: make him get out of debt on his own. Encourage him for sure. But don’t do it for him. That’s his test.

Look, I’ve been doing this a long time. I meet a lot of people who have shacked up with a partner thinking they’ll change them. Most of the time it doesn’t work. Especially when it comes to money management. Then again, I could be wrong, I’ve never encountered a knight!

Scott